Budgeting can feel overwhelming when you first start managing your money.

Many people struggle because they:

- Overcomplicate budgeting

- Track too many categories

- Create unrealistic spending limits

That’s why the 50/30/20 rule became one of the most popular budgeting methods in the USA.

It’s simple, beginner-friendly, and easy to follow.

In this guide, you’ll learn:

- What the 50/30/20 rule is

- How it works

- Real US budgeting examples

- Benefits and disadvantages

- How to apply it to your income

By the end, you’ll know exactly how to create a realistic monthly budget.

🔥 QUICK ANSWER

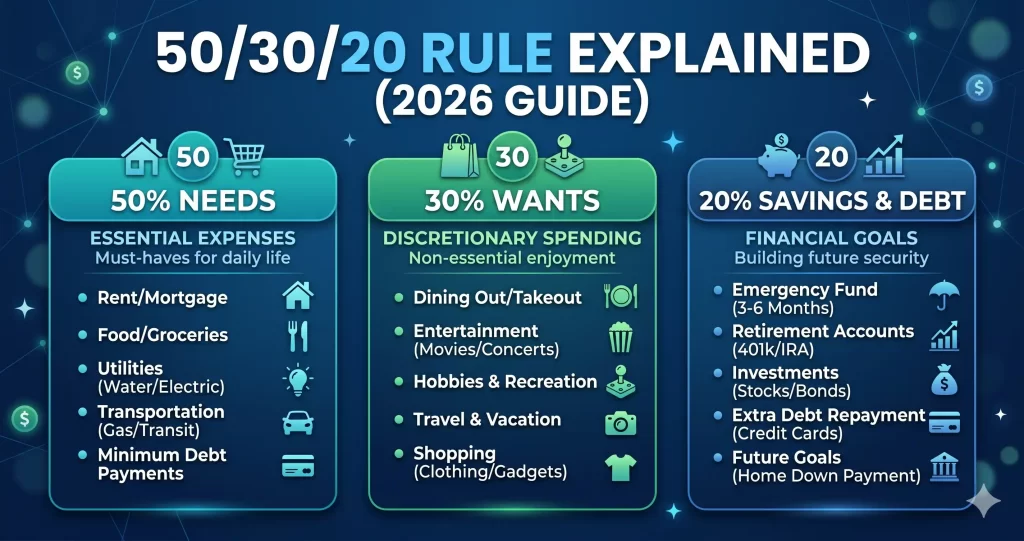

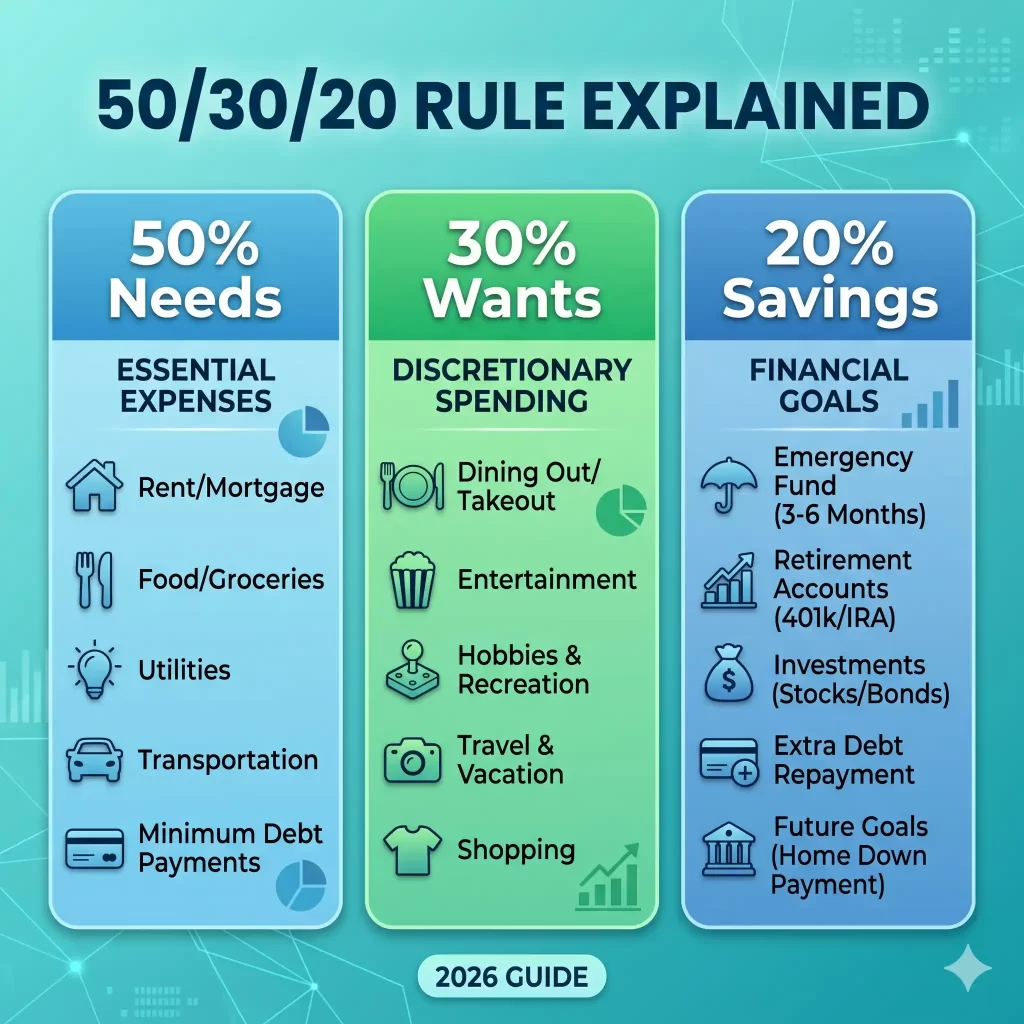

The 50/30/20 rule is a budgeting method where:

- 50% of income goes to needs

- 30% goes to wants

- 20% goes to savings and debt repayment

👉 It’s one of the easiest budgeting systems for beginners.

📊 WHAT IS THE 50/30/20 RULE?

The 50/30/20 rule divides your after-tax income into three categories.

💵 50% → NEEDS

Needs are essential expenses required for living.

Examples:

- Rent or mortgage

- Utilities

- Groceries

- Transportation

- Insurance

- Minimum debt payments

👉 These are expenses you cannot easily avoid.

🛍 30% → WANTS

Wants are non-essential lifestyle expenses.

Examples:

- Streaming services

- Dining out

- Shopping

- Vacations

- Entertainment

👉 Wants improve lifestyle but aren’t necessary for survival.

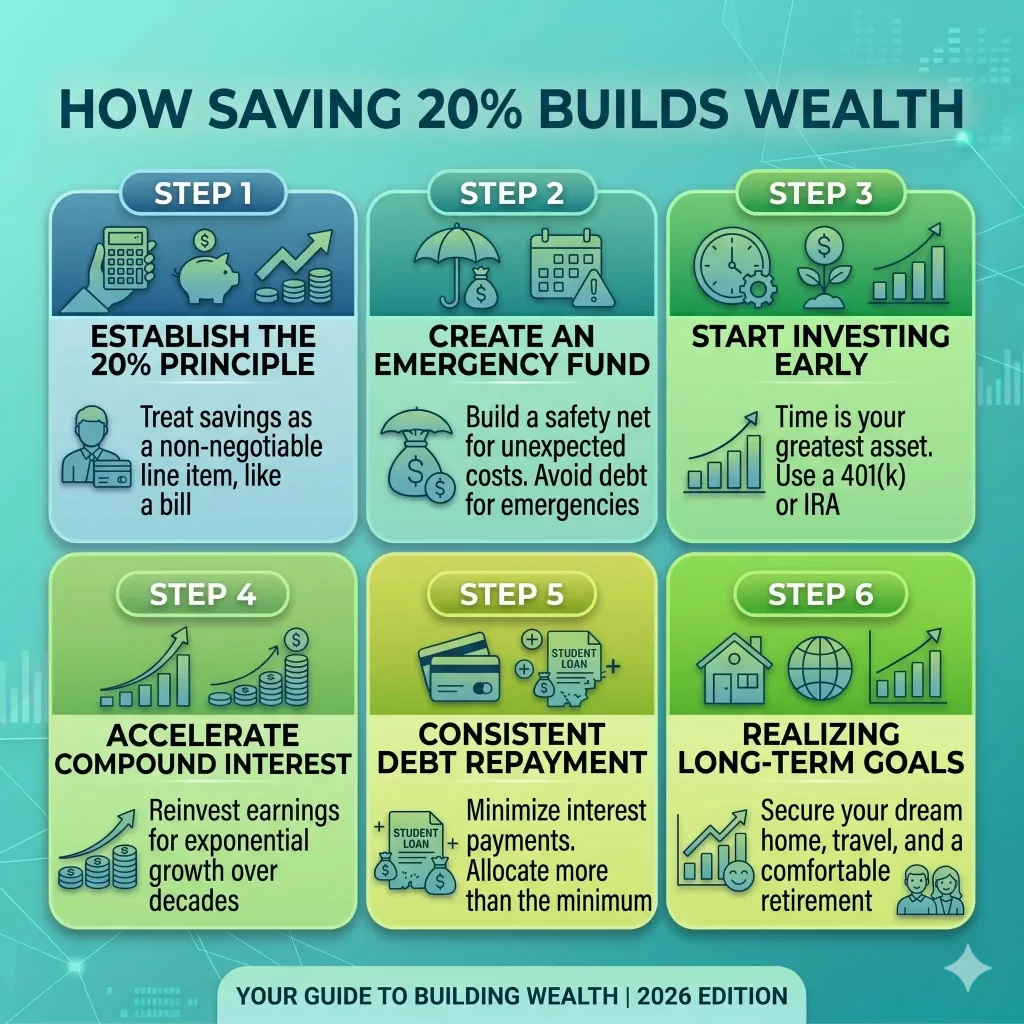

💰 20% → SAVINGS & DEBT PAYOFF

This category focuses on financial growth and stability.

Examples:

- Emergency fund

- Retirement savings

- Investments

- Extra debt payments

👉 This is where long-term financial security is built.

📈 WHY THE 50/30/20 RULE IS SO POPULAR

The 50/30/20 method is popular because it’s:

✅ Simple

✅ Flexible

✅ Beginner-friendly

✅ Realistic for most households

Unlike strict budgeting systems, it allows room for enjoyment while still encouraging saving.

💡 REAL US EXAMPLE OF THE 50/30/20 RULE

Example Monthly Income:

$4,000 after taxes

🔹 Needs (50%)

Budget:

$2,000

Expenses:

- Rent → $1,200

- Utilities → $200

- Groceries → $400

- Transportation → $200

🔹 Wants (30%)

Budget:

$1,200

Expenses:

- Restaurants → $300

- Streaming → $50

- Shopping → $300

- Entertainment → $250

- Travel savings → $300

🔹 Savings & Debt (20%)

Budget:

$800

Uses:

- Emergency fund → $300

- Retirement → $300

- Extra debt payment → $200

👉 This creates a balanced financial plan.

🚀 HOW TO START USING THE 50/30/20 RULE

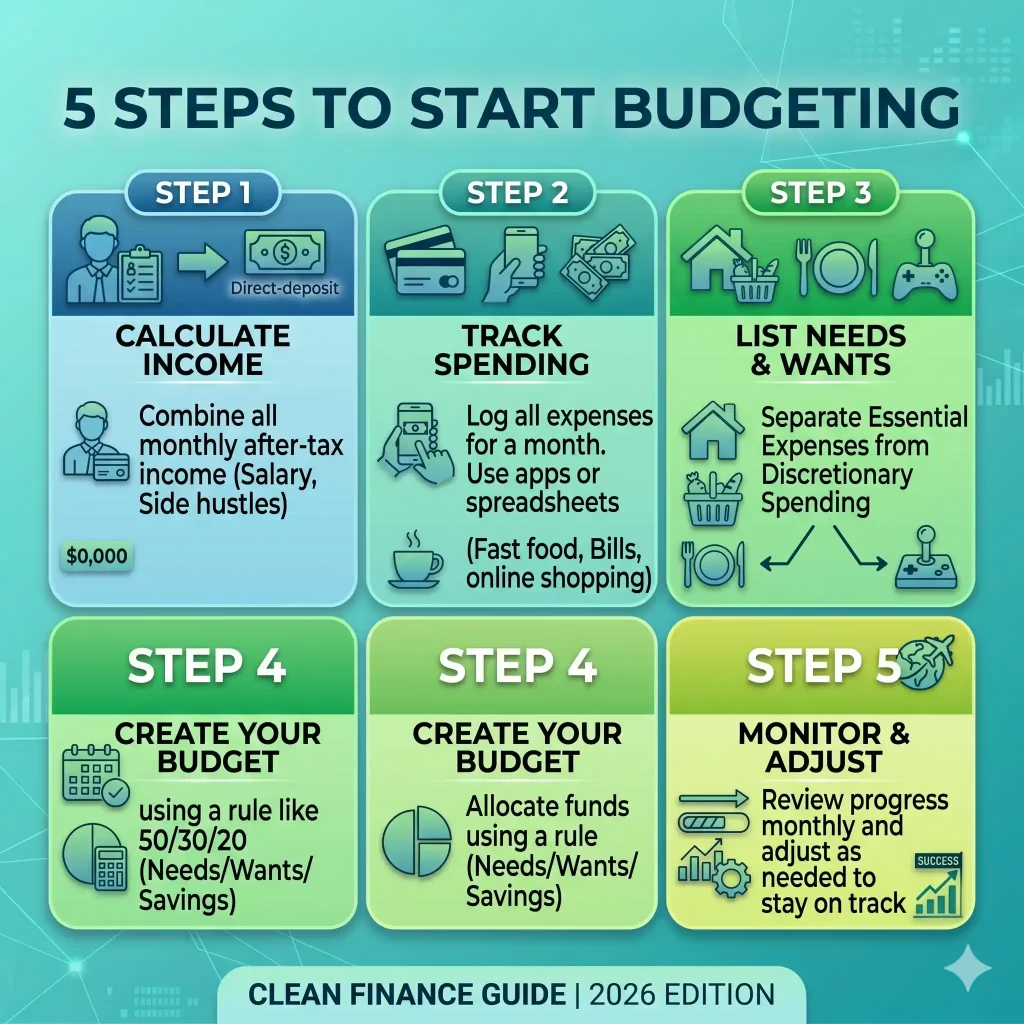

Step 1: Calculate After-Tax Income

Use your take-home pay after:

- Taxes

- Insurance

- Retirement deductions

👉 Accurate income calculation is important.

Step 2: Track Current Expenses

Review:

- Bank statements

- Credit card transactions

- Monthly bills

👉 Many people underestimate spending.

Step 3: Categorize Spending

Split all expenses into:

- Needs

- Wants

- Savings

👉 This reveals spending habits quickly.

Step 4: Adjust Spending

If your “wants” exceed 30%, reduce:

- Dining out

- Shopping

- Subscriptions

Step 5: Automate Savings

Set automatic transfers to:

- Savings accounts

- Investment accounts

👉 Automation improves consistency.

⚡ BENEFITS OF THE 50/30/20 RULE

✅ Easy to understand

No complicated spreadsheets required.

✅ Helps reduce overspending

Spending categories create accountability.

✅ Encourages saving

The 20% category prioritizes financial growth.

✅ Flexible lifestyle budgeting

You can still enjoy entertainment and hobbies.

⚠️ DISADVANTAGES OF THE 50/30/20 RULE

❌ Difficult in high-cost cities

Rent may exceed 50% in some US cities.

❌ Doesn’t fit every income level

Low-income households may struggle to save 20%.

❌ Requires self-discipline

The system only works if you follow it consistently.

📊 HOW TO ADAPT THE RULE FOR LOW INCOME

If your expenses are high:

👉 Modify percentages temporarily.

Example:

- Needs → 60%

- Wants → 20%

- Savings → 20%

👉 The goal is progress, not perfection.

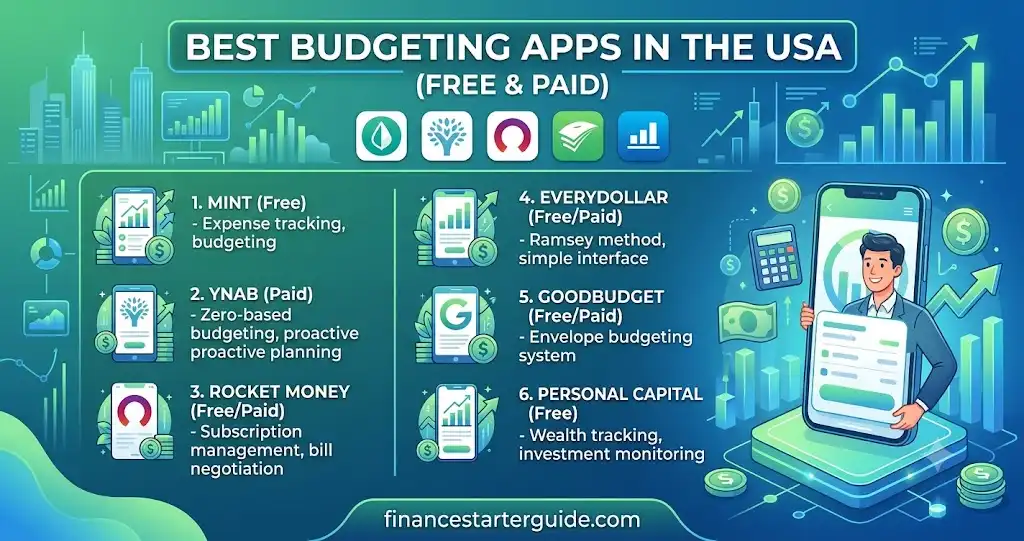

💸 BEST TOOLS FOR THE 50/30/20 RULE

You can use:

- Budgeting apps

- Spreadsheets

- Banking apps

- Expense trackers

👉 Digital tools make budgeting easier.

📱 BEST BUDGETING APPS FOR THIS METHOD

Useful features include:

- Expense categories

- Spending alerts

- Savings tracking

👉 Automation helps maintain consistency.

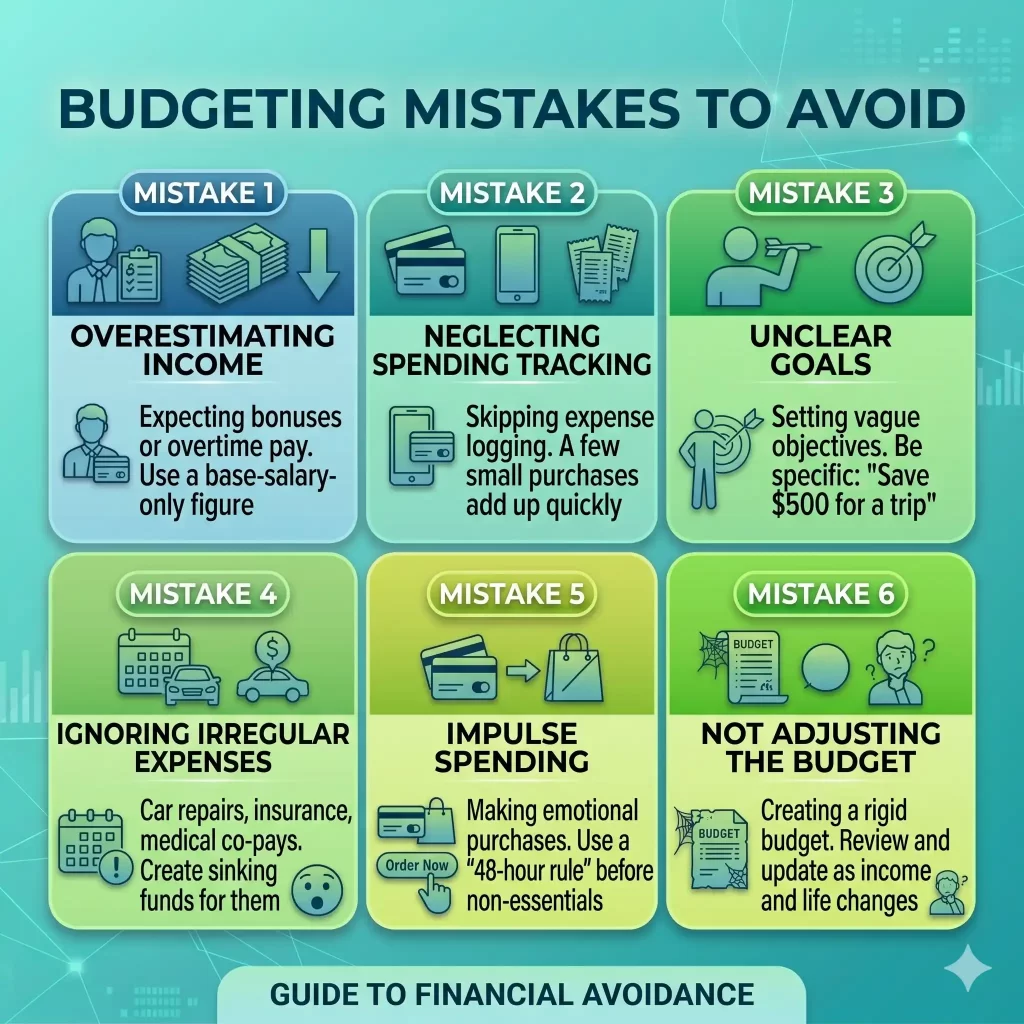

🔥 COMMON MISTAKES PEOPLE MAKE

❌ Misclassifying wants as needs

Examples:

- Expensive dining

- Luxury shopping

❌ Ignoring irregular expenses

Examples:

- Car repairs

- Medical bills

- Holidays

❌ Not reviewing budgets monthly

Financial situations change regularly.

❌ Saving only leftover money

Savings should be planned first.

🏦 HOW THE 50/30/20 RULE HELPS BUILD WEALTH

Long-term saving creates:

- Emergency funds

- Investment growth

- Reduced financial stress

👉 Small monthly savings compound significantly over time.

💳 HOW THIS RULE IMPROVES CREDIT SCORE

Good budgeting helps:

- Avoid late payments

- Reduce credit card debt

- Lower credit utilization

👉 Financial organization improves credit health.

📈 50/30/20 RULE VS OTHER BUDGETING METHODS

| Method | Best For |

|---|---|

| 50/30/20 | Beginners |

| Zero-based budgeting | Detailed planners |

| Envelope system | Cash spenders |

| Pay yourself first | Saving-focused users |

👉 The 50/30/20 rule is the easiest starting point.

🧠 FAQ SECTION

What is the 50/30/20 rule?

The 50/30/20 rule is a budgeting method dividing income into needs, wants, and savings.

Is the 50/30/20 rule good for beginners?

Yes, it’s one of the easiest budgeting systems for beginners.

Does the 50/30/20 rule work on low income?

Yes, but percentages may need adjustment based on expenses.

What counts as needs in the 50/30/20 rule?

Needs include rent, groceries, utilities, transportation, and insurance.

Can the 50/30/20 rule help save money?

Yes, it encourages consistent saving and spending awareness.

- What is a budget?

- Best budgeting apps in the USA

- How to save money fast

- How to improve credit score fast

🏆 FINAL THOUGHTS

The 50/30/20 rule is one of the best budgeting systems for beginners because it’s simple, realistic, and effective.

You don’t need perfect finances to start budgeting successfully.

👉 Focus on:

- Awareness

- Consistency

- Long-term habits

Small financial improvements create major long-term results.

Disclaimer: This article is for educational and informational purposes only and does not constitute financial, investment, tax, or legal advice.

Pingback: Top 15 Money Saving Tips That Actually Work in the USA (2026 Guide)

Pingback: Best Budgeting Apps in the USA (Free & Paid) 2026 Guide - Finance Starter Guide

Pingback: How to Save Money Fast on a Low Income (USA Guide 2026)

Pingback: How to Save $1000 Fast (Realistic Plan for Beginners USA 2026)

Pingback: Emergency Fund: How Much Do You Really Need? (USA Guide 2026)

Pingback: How to Track Expenses Effectively (Free Methods)

Pingback: How Millennials Can Build Wealth from Scratch (Complete 2026 Guide)