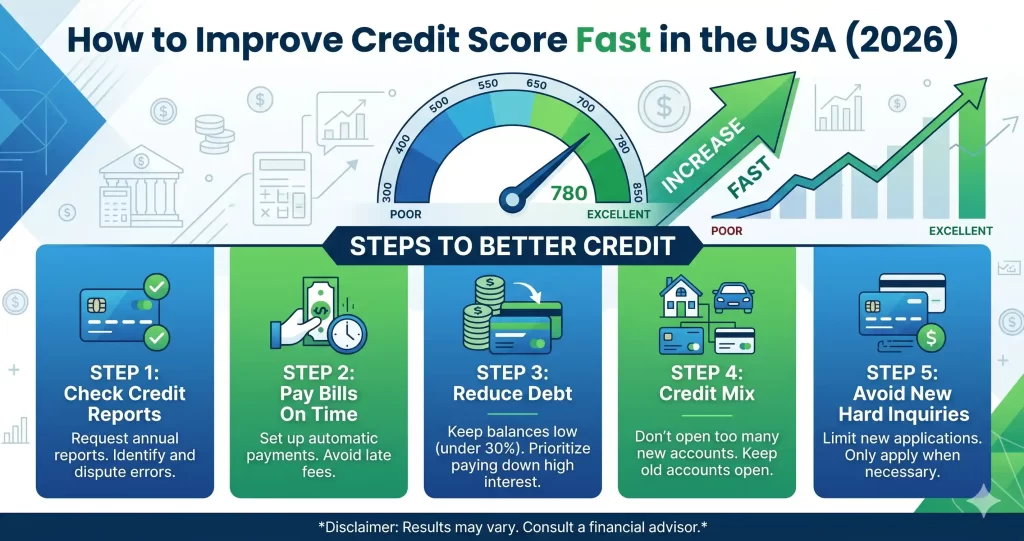

If you want to improve your credit score fast, there’s one factor you should focus on immediately:

It’s one of the fastest ways to boost your score sometimes within 30 days.

But many people don’t fully understand:

- What credit utilization is

- How it works

- How to optimize it

This guide explains everything in simple terms so you can start improving your credit score today.

🔥 QUICK ANSWER

Credit utilization is the percentage of your available credit that you are currently using.

👉 Example:

If your limit is $1,000 and you use $300 → your utilization is 30%

Best practice: Keep utilization below 30% (ideally under 10%) to improve your credit score.

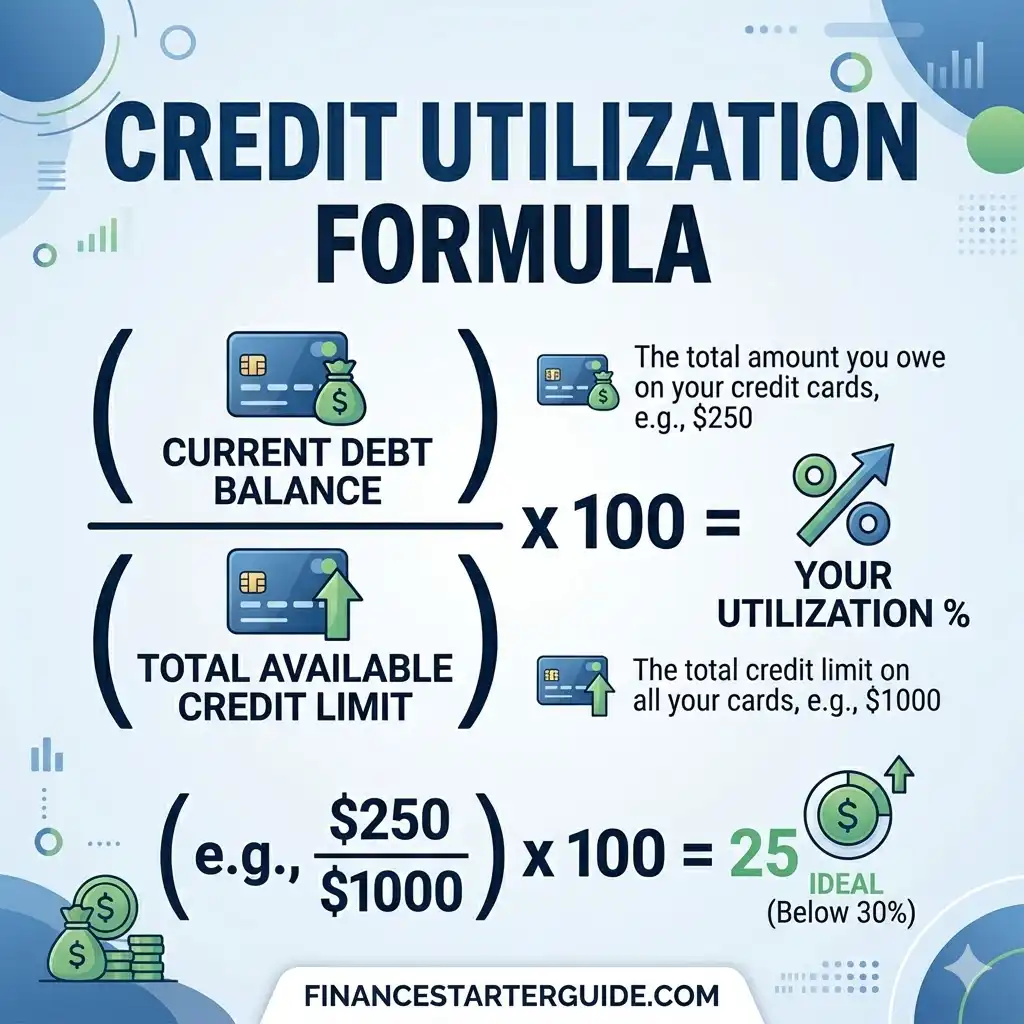

📊 WHAT IS CREDIT UTILIZATION?

Credit utilization (also called credit usage ratio) measures how much of your credit limit you are using.

📌 Formula:

Credit Utilization = (Used Credit ÷ Total Credit Limit) × 100

💡 Example:

- Total limit: $5,000

- Balance: $1,000

👉 Utilization = 20%

👉 Lower utilization = better credit score

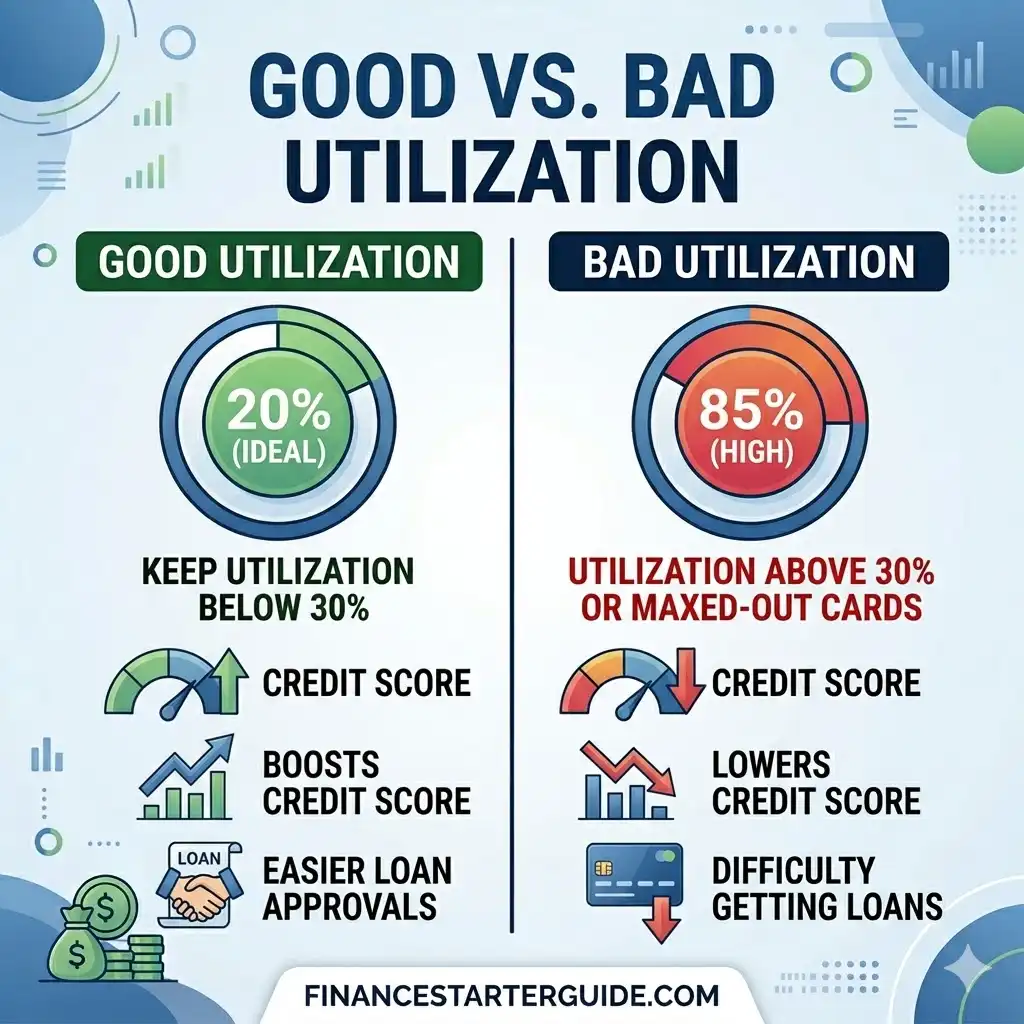

📈 WHY CREDIT UTILIZATION MATTERS

Credit utilization makes up about 30% of your credit score.

That means:

- It’s the second most important factor

- It has a fast impact on your score

👉 Small changes can lead to quick improvements.

💳 HOW UTILIZATION AFFECTS YOUR CREDIT SCORE

| Utilization | Impact |

|---|---|

| 0–10% | Excellent |

| 10–30% | Good |

| 30–50% | Risky |

| 50%+ | Poor |

| 80%+ | Very harmful |

👉 Crossing 30% is where your score starts dropping.

🚨 COMMON MISTAKE: THINKING 0% IS BEST

Using 0% credit is not always ideal.

👉 Why?

- Credit scoring models want to see activity

- No usage = no data

👉 Best range: 1%–10% utilization

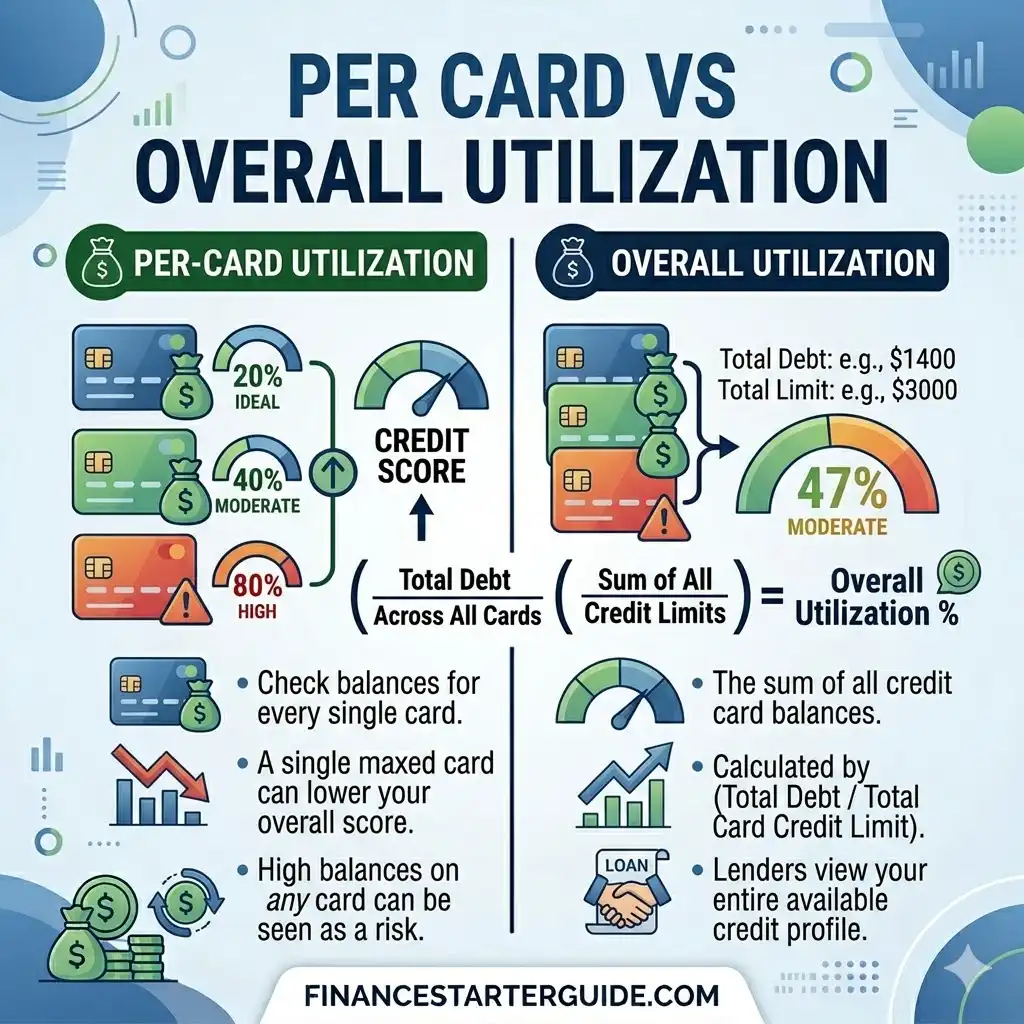

📊 PER CARD VS OVERALL UTILIZATION

There are two types of utilization:

🔹 Overall Utilization

Total balances ÷ total credit limits

🔹 Per Card Utilization

Balance on each card ÷ that card’s limit

👉 Both matter.

Example:

- Card A: 90% used ❌

- Card B: 0% used

👉 Still hurts your score

⚡ FASTEST WAY TO BOOST YOUR SCORE

Credit utilization is one of the fastest ways to improve credit score.

💡 Why?

Because:

- It updates monthly

- Changes reflect quickly

👉 You can see results in 30 days

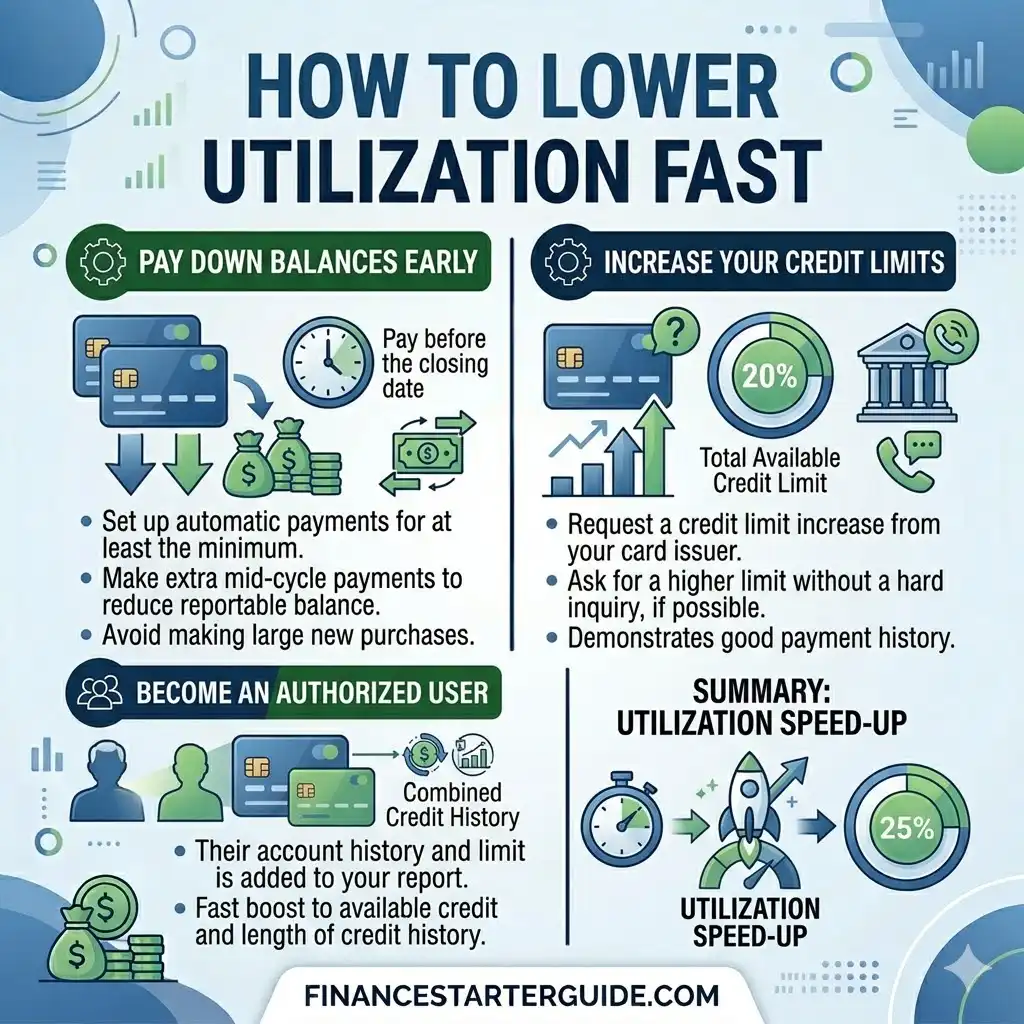

🚀 HOW TO LOWER CREDIT UTILIZATION FAST

✅ Pay Down Balances

The most effective method.

👉 Pay as much as possible before statement date.

✅ Make Multiple Payments Monthly

Instead of paying once:

👉 Pay weekly or bi-weekly

✅ Request Credit Limit Increase

Higher limit = lower utilization

👉 Don’t increase spending after.

✅ Open a New Credit Card (Carefully)

Increases total available credit

👉 Only if you can manage it responsibly.

✅ Spread Balances Across Cards

Avoid maxing out one card.

📅 STATEMENT DATE VS DUE DATE (IMPORTANT)

Many people make this mistake.

📌 Statement Date

Balance reported to credit bureaus

📌 Due Date

When payment is required

👉 To optimize utilization:

Pay BEFORE the statement date

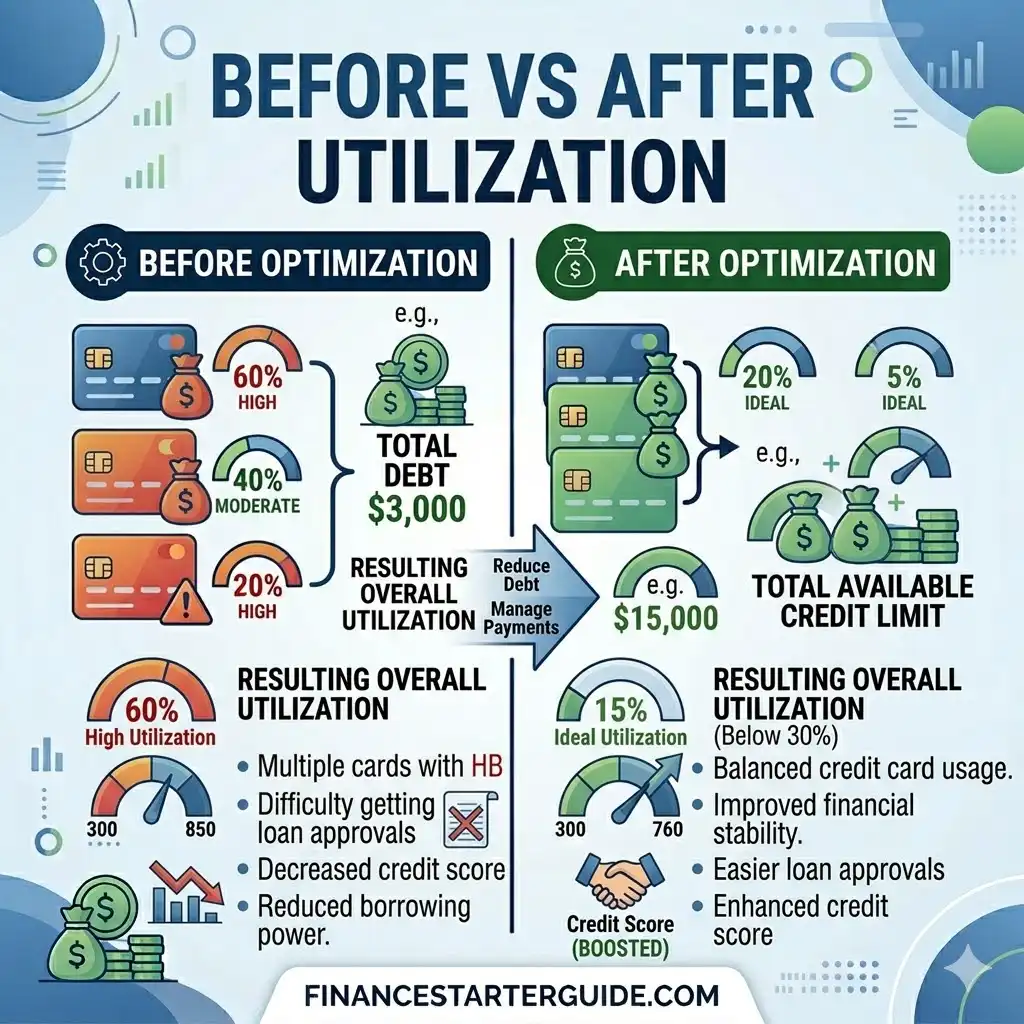

📊 REAL EXAMPLE (USA)

Before:

- Limit: $2,000

- Balance: $1,200

👉 Utilization: 60%

Score: Low

After:

- Balance reduced to $300

👉 Utilization: 15%

👉 Score increases within 30–45 days

💸 IDEAL CREDIT UTILIZATION STRATEGY

Beginner Strategy:

- Keep usage under 30%

Advanced Strategy:

- Keep usage under 10%

Expert Strategy:

- Use 1–5% for maximum optimization

👉 Lower = better (but not zero)

⚠️ WHAT HURTS YOUR UTILIZATION

❌ Maxing out cards

❌ Carrying high balances

❌ Only paying minimums

❌ Ignoring statement dates

👉 These can drop your score quickly.

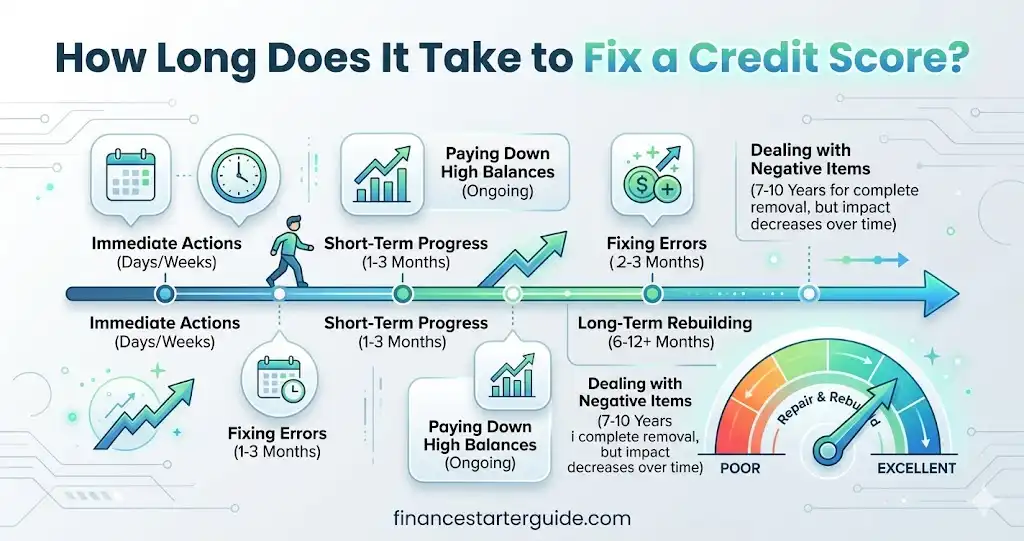

📈 HOW FAST UTILIZATION CHANGES YOUR SCORE

- 7–30 days → visible improvement

- 1–2 billing cycles → strong boost

👉 It’s the fastest credit factor to optimize.

💳 UTILIZATION VS DEBT (IMPORTANT DIFFERENCE)

Utilization = Ratio

Debt = Total amount owed

👉 You can:

- Have high debt but low utilization (good)

- Have low debt but high utilization (bad)

🧠 BEST PRACTICES FOR LONG-TERM SUCCESS

✅ Always pay in full when possible

✅ Keep balances low

✅ Monitor accounts regularly

✅ Avoid unnecessary spending

✅ Increase limits over time

🔥 CREDIT UTILIZATION HACKS

💡 Pay Before Statement Closing

Reduces reported balance

💡 Use Multiple Cards

Keeps per-card usage low

💡 Small Purchases Only

Keeps utilization minimal

💡 Set Alerts

Avoid high usage

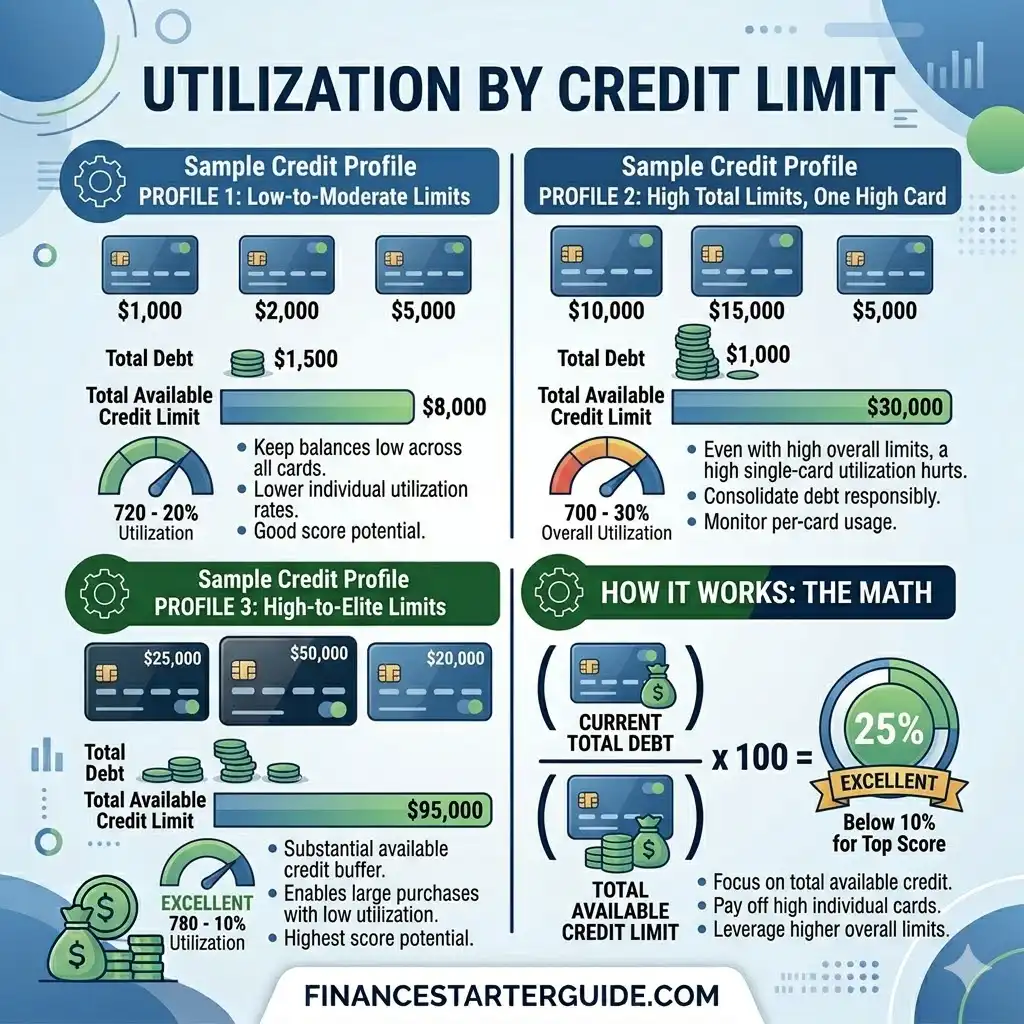

📊 UTILIZATION FOR DIFFERENT CREDIT LIMITS

$500 Limit

Keep usage under $50

$1,000 Limit

Keep usage under $100

$5,000 Limit

Keep usage under $500

👉 Same percentage rule applies.

🏦 DOES UTILIZATION RESET EVERY MONTH?

Yes.

👉 It is recalculated monthly

This means:

- You can fix mistakes quickly

- You can improve score repeatedly

📉 WHAT IF YOUR UTILIZATION IS HIGH?

Don’t panic.

Step-by-step fix:

- Pay down balances

- Stop new spending

- Increase limits

- Monitor progress

👉 Improvements start within weeks.

📈 HOW MUCH CAN YOUR SCORE INCREASE?

- Small changes → +20–40 points

- Big reductions → +50–100 points

👉 Depends on your starting score.

🧠 FAQ SECTION

What is credit utilization?

Credit utilization is the percentage of your credit limit that you are using.

What is a good credit utilization ratio?

A good ratio is below 30%, ideally under 10%.

Does lowering utilization increase credit score?

Yes, lowering utilization can quickly improve your credit score.

How fast does utilization affect credit score?

Changes can impact your score within 30 days.

Is 0% utilization good?

Not always small usage (1–10%) is better.

- What is a credit score

- How to fix a credit score

- Best secured credit cards USA

- How to save money fast

Disclaimer: This article is for educational and informational purposes only and does not constitute financial, investment, tax, or legal advice.

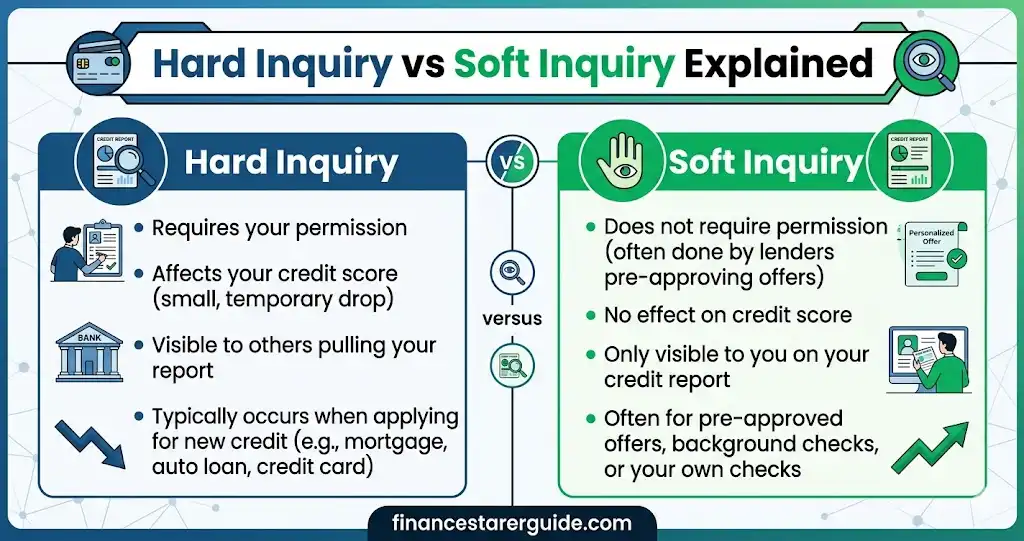

Pingback: Hard Inquiry vs Soft Inquiry (Full Guide) USA Credit Score 2026

Pingback: Debt Snowball vs Debt Avalanche (Which Is Better?)

Pingback: Best 0% APR Credit Cards in the USA (2026 Guide)