Financial success isn’t built by making one perfect money decision it’s built through consistent habits repeated over time.

Whether your goal is to save for a home, eliminate debt, invest for retirement, or simply stop worrying about money, developing strong financial habits is one of the best investments you can make.

The challenge isn’t knowing what to do it’s sticking with it.

This guide explains how to build good financial habits that last, avoid common mistakes, and create a financial system that works automatically.

🔥 Quick Answer

How Do You Build Good Financial Habits That Stick?

To build lasting financial habits:

- Create a realistic monthly budget.

- Automate savings.

- Track your spending.

- Pay bills on time.

- Build an emergency fund.

- Invest consistently.

- Avoid lifestyle inflation.

- Review your finances monthly.

- Set achievable financial goals.

- Focus on consistency instead of perfection.

Small daily actions become powerful long-term financial habits.

Why Financial Habits Matter

Good habits help you:

- Spend less than you earn

- Reduce financial stress

- Build savings faster

- Improve your credit score

- Reach financial goals sooner

- Create long-term wealth

Financial freedom is usually the result of consistent habits not sudden windfalls.

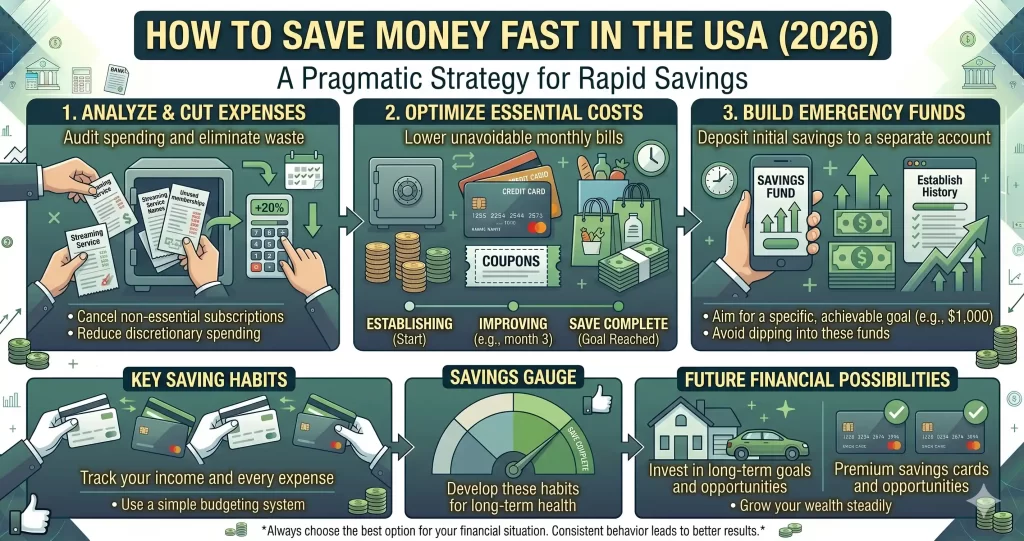

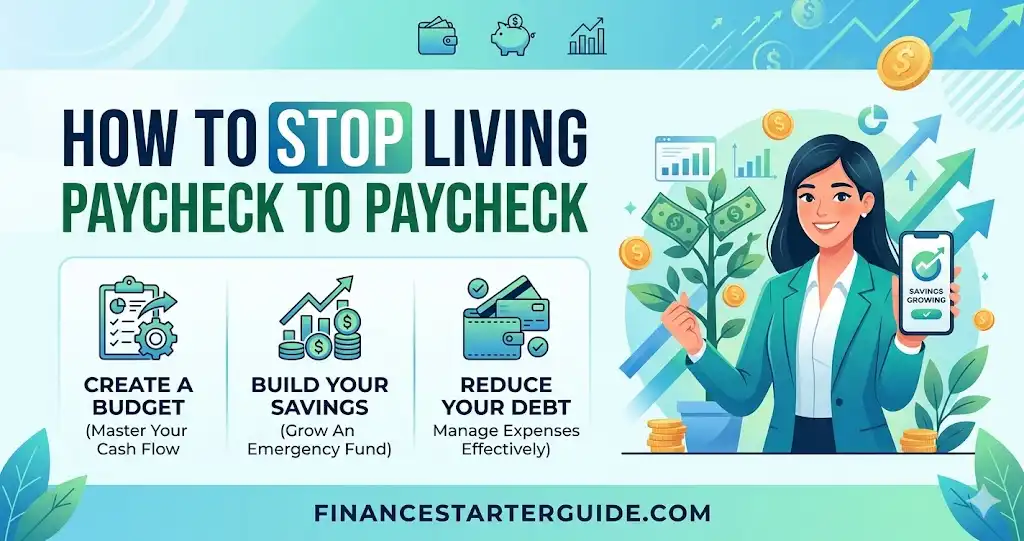

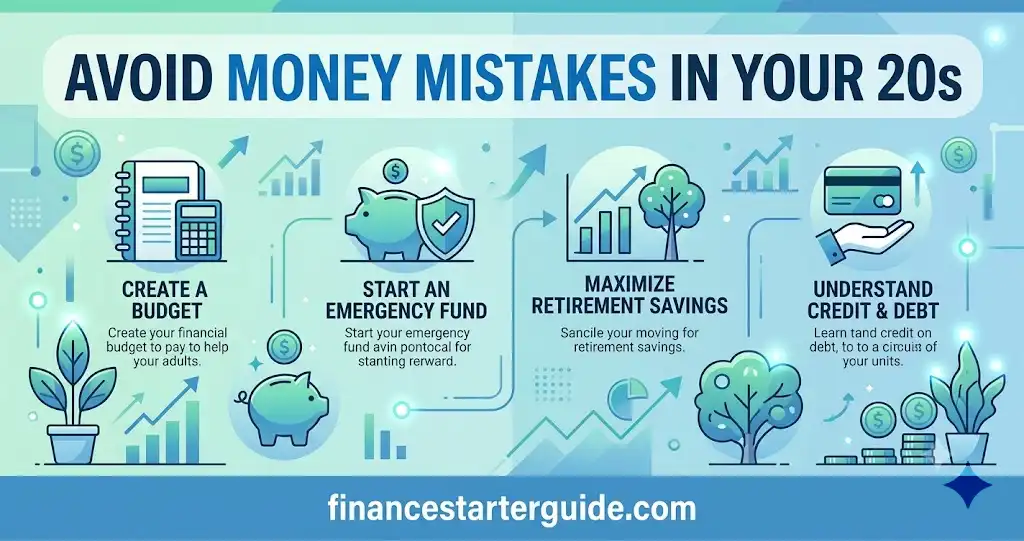

Habit #1: Create a Monthly Budget

A budget tells your money where to go before you spend it.

Popular budgeting methods include:

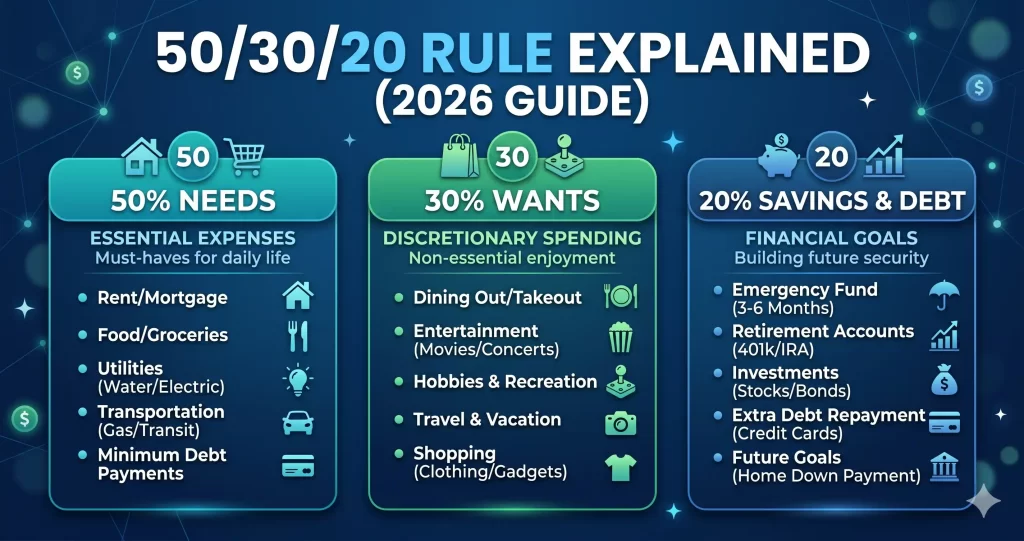

- 50/30/20 Rule

- Zero-Based Budget

- Envelope Budgeting

A simple budget helps you:

- Control spending

- Increase savings

- Reduce unnecessary purchases

Habit #2: Pay Yourself First

Before spending money:

✔ Save first

✔ Invest first

✔ Spend what’s left

Automating transfers into savings immediately after payday makes this habit easier to maintain.

Habit #3: Track Every Dollar

You cannot improve what you don’t measure.

Track:

- Housing

- Transportation

- Food

- Entertainment

- Shopping

- Subscriptions

Many budgeting apps make expense tracking simple.

Habit #4: Build an Emergency Fund

Unexpected expenses happen.

Examples:

- Medical emergencies

- Car repairs

- Job loss

- Home maintenance

Aim for:

- First milestone: $1,000

- Long-term goal: 3–6 months of essential expenses

Habit #5: Avoid Lifestyle Inflation

As your income grows, don’t increase spending at the same rate.

Instead:

- Increase savings

- Invest more

- Pay off debt

- Build wealth

This habit creates long-term financial stability.

Habit #6: Use Credit Responsibly

Credit cards can be valuable financial tools when used wisely.

Best practices:

- Pay on time

- Pay in full whenever possible

- Keep balances low

- Avoid unnecessary debt

Responsible credit use can strengthen your credit history over time.

Habit #7: Automate Your Finances

Automation removes the temptation to skip good habits.

Automate:

- Savings

- Investments

- Bill payments

- Retirement contributions

This reduces missed payments and keeps your goals on track.

Habit #8: Invest Consistently

Many people delay investing because they believe they need a large amount of money.

Starting with small, regular contributions can help build wealth over time.

Focus on consistency rather than trying to time the market.

Habit #9: Review Your Finances Monthly

Once every month:

- Review your budget

- Check account balances

- Monitor savings goals

- Review investments

- Check subscriptions

- Adjust your budget

A monthly review helps catch problems before they become expensive.

Habit #10: Continue Learning

Financial education never ends.

Read:

- Personal finance books

- Trusted financial blogs

- Educational articles

- Government financial resources

The more you learn, the better your financial decisions become.

30-Day Financial Habits Challenge

Week 1

- Create a budget

- Track spending

Week 2

- Build emergency savings

- Cancel unnecessary subscriptions

Week 3

- Automate savings

- Review debt

Week 4

- Review goals

- Increase savings if possible

After 30 days, these actions begin to feel more natural.

Daily Financial Habits Checklist

✔ Check your spending

✔ Avoid impulse purchases

✔ Save a little money

✔ Stick to your budget

✔ Review financial goals

✔ Learn one new money tip

Consistency is more important than perfection.

Common Financial Habits That Hurt Your Money

Avoid these mistakes:

- Spending without a budget

- Ignoring savings

- Carrying credit card balances

- Missing bill payments

- Emotional spending

- Lifestyle inflation

- Not investing

- Ignoring financial goals

Replacing one bad habit at a time is usually more sustainable than trying to change everything at once.

FAQs

What are good financial habits?

Good financial habits include budgeting, saving regularly, paying bills on time, investing consistently, tracking expenses, and avoiding unnecessary debt.

How long does it take to build a financial habit?

The exact timeline varies from person to person, but repeating the behavior consistently over weeks and months increases the likelihood that it becomes routine.

Why are financial habits important?

Strong financial habits help reduce stress, improve savings, manage debt, and support long-term wealth building.

What is the best financial habit for beginners?

Creating a budget and paying yourself first are two of the most effective habits for beginners.

Can small habits really build wealth?

Yes. Small, consistent actions such as saving monthly and investing regularly can make a significant difference over many years.

Conclusion

Building good financial habits isn’t about being perfect it’s about being consistent.

Start with one habit, practice it daily, and gradually add new ones as your confidence grows.

Remember:

- Budget every month.

- Save before spending.

- Invest consistently.

- Review your finances regularly.

- Keep learning.

These simple habits can help you build a stronger financial future one step at a time.

- What Is a Budget? (USA Beginner Guide)

- 50/30/20 Rule Explained

- How to Track Expenses Effectively

- How to Avoid Common Money Mistakes in Your 20s

- Emergency Fund: How Much Do You Really Need?

- Best Budgeting Apps in the USA

- How Millennials Can Build Wealth from Scratch

- Best Side Hustles to Save More Money

Disclaimer: This article is for educational and informational purposes only and does not constitute financial, investment, tax, or legal advice.