Your 20s are one of the most important decades for building a strong financial future. The money habits you develop now can influence your finances for decades to come.

Unfortunately, many young adults make financial mistakes that delay wealth building, increase debt, and create unnecessary stress. The good news is that most of these mistakes are preventable.

Whether you’re starting your first job, graduating from college, or simply trying to improve your finances, this guide will show you how to avoid the most common money mistakes in your 20s and build a solid financial foundation.

🔥 Quick Answer

How Can You Avoid Common Money Mistakes in Your 20s?

To avoid common money mistakes in your 20s:

- Create and follow a monthly budget.

- Build an emergency fund.

- Avoid unnecessary debt.

- Pay credit card balances on time.

- Start investing early.

- Improve your credit score.

- Track your expenses.

- Live below your means.

- Set financial goals.

- Continue learning about personal finance.

These habits can help you build wealth and reduce financial stress over time.

Why Your 20s Matter Financially

Your 20s provide a unique advantage because time allows your savings and investments to grow through compound growth.

Starting early can mean:

- More investment growth

- Better credit history

- Lower financial stress

- Greater financial freedom

- More retirement savings

Even small monthly contributions can grow significantly over many years.

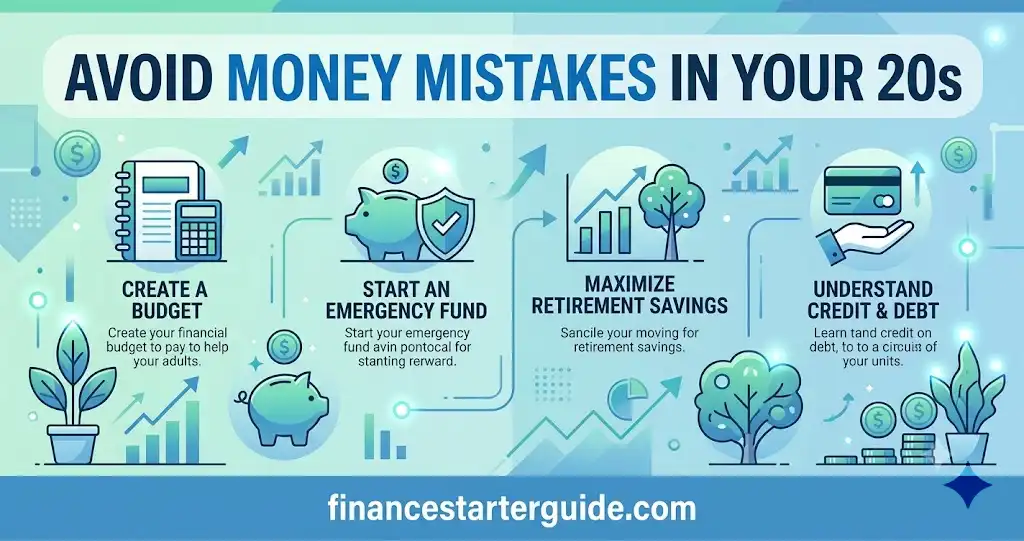

Money Mistake #1: Not Having a Budget

One of the biggest financial mistakes is spending without a plan.

A budget helps you:

- Control spending

- Save consistently

- Avoid debt

- Reach financial goals

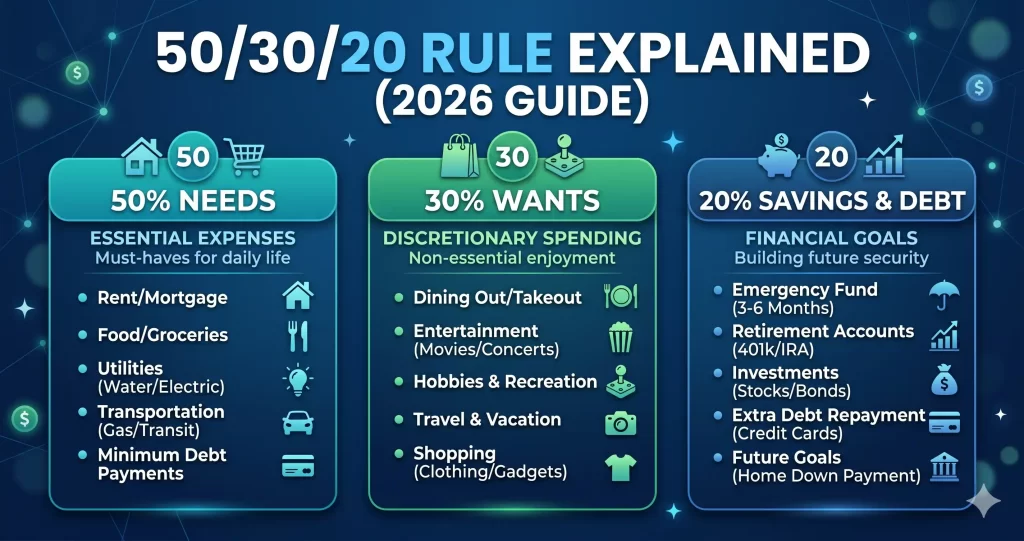

Try the 50/30/20 Rule

- 50% Needs

- 30% Wants

- 20% Savings and debt repayment

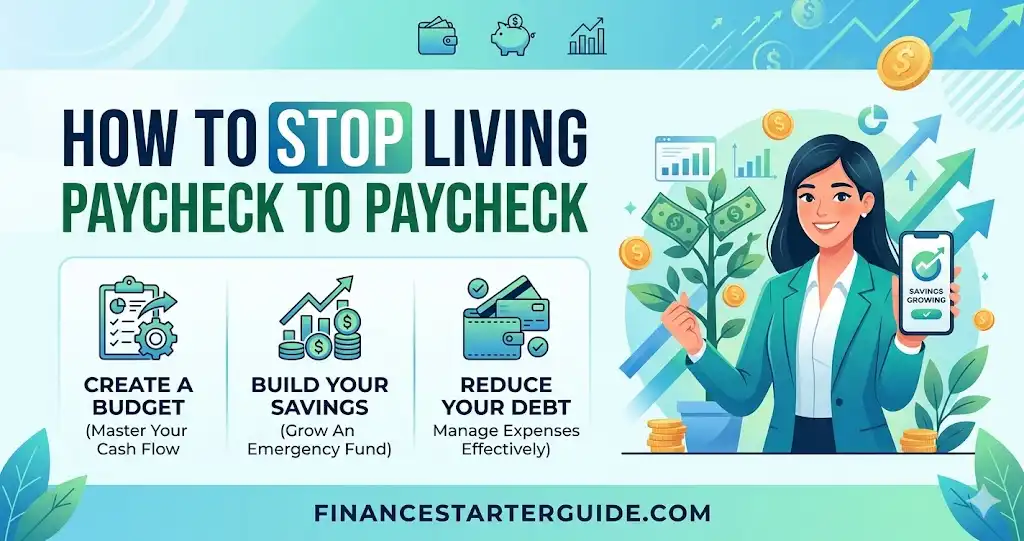

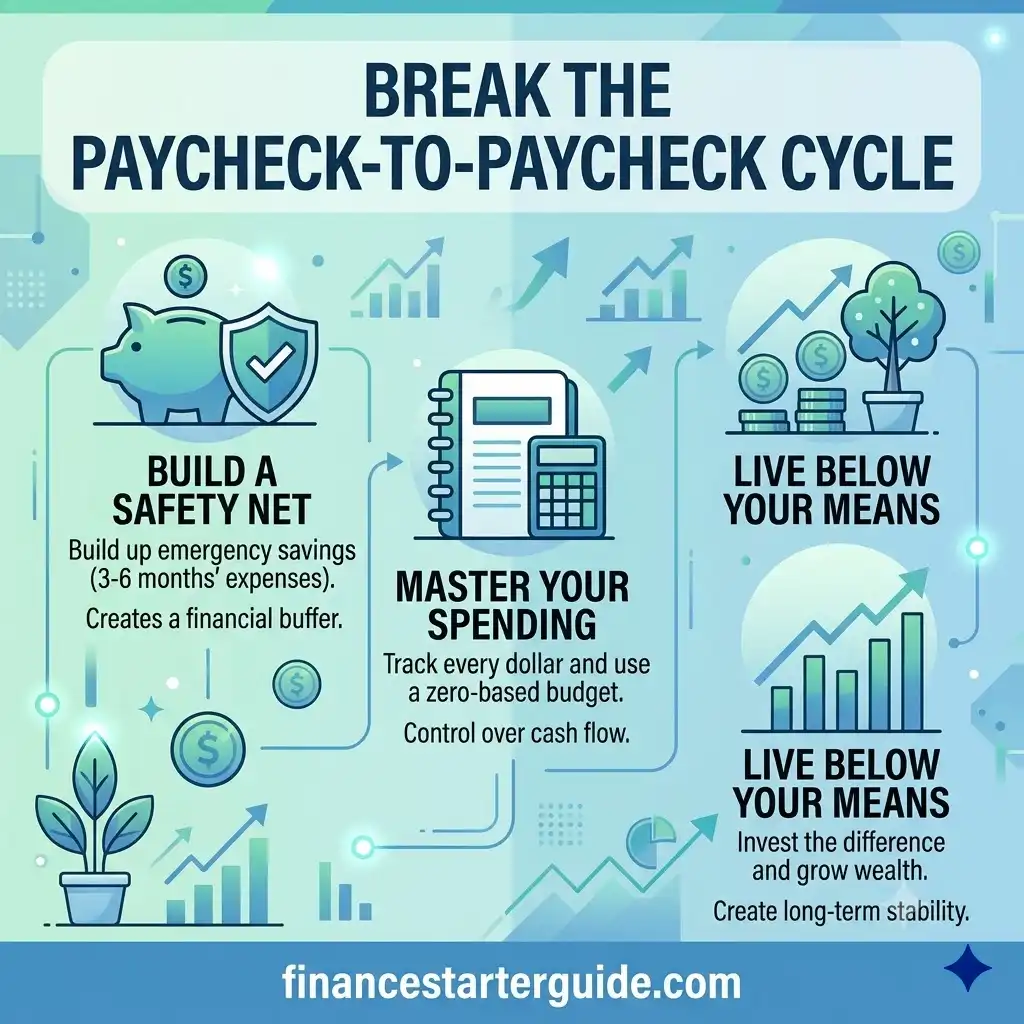

Money Mistake #2: Living Paycheck to Paycheck

Many young adults spend every dollar they earn.

Instead:

- Save first

- Automate savings

- Increase your savings rate whenever your income grows

Even saving $100–$200 per month can make a significant difference over time.

Money Mistake #3: Ignoring an Emergency Fund

Unexpected expenses happen.

Examples include:

- Medical bills

- Car repairs

- Job loss

- Home repairs

Aim to save:

- Starter fund: $1,000

- Long-term goal: 3–6 months of living expenses

A high-yield savings account can be a good place to keep emergency savings.

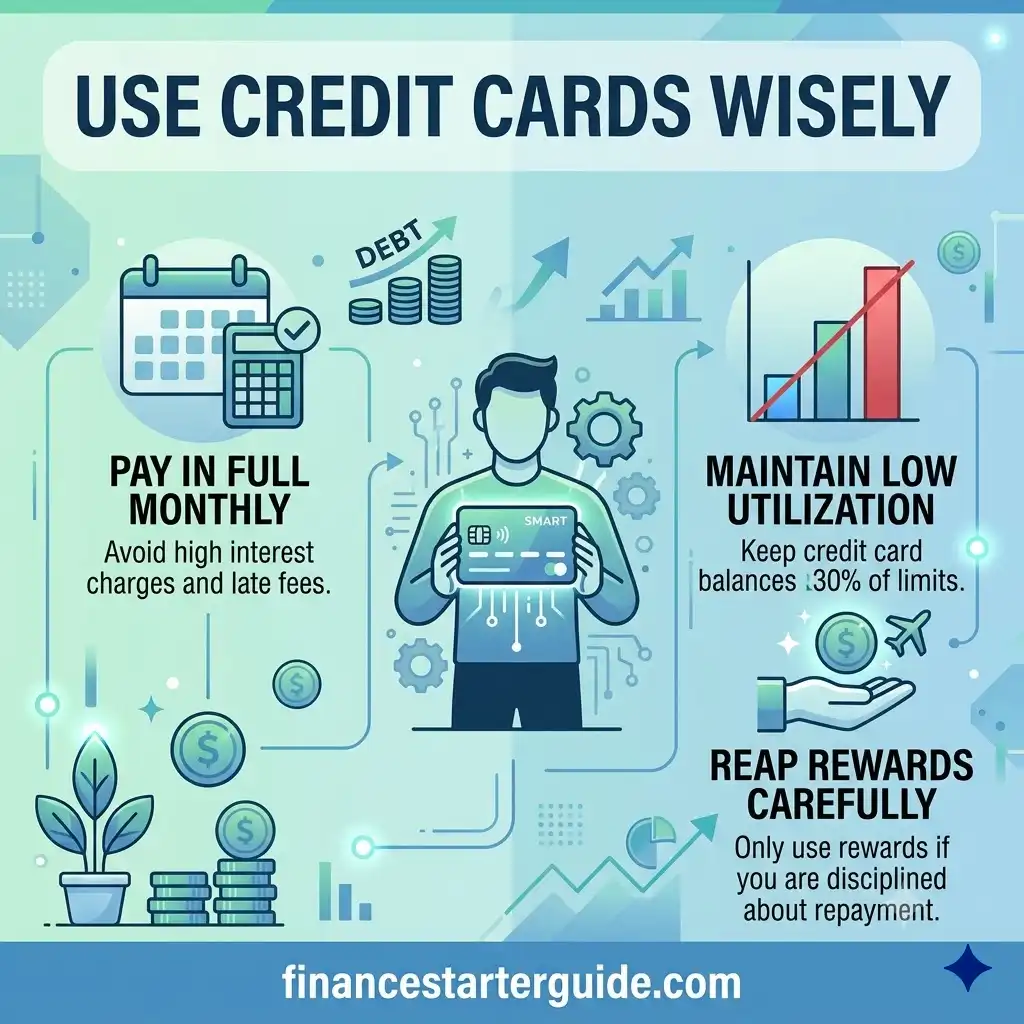

Money Mistake #4: Misusing Credit Cards

Credit cards can be helpful when used responsibly.

Avoid:

- Carrying high balances

- Missing payments

- Maxing out your credit limit

Best practices:

- Pay your balance in full whenever possible.

- Pay on time every month.

- Keep credit utilization low.

Money Mistake #5: Waiting Too Long to Invest

Many people believe investing requires a lot of money.

In reality, many platforms allow beginners to start with small amounts.

Benefits of investing early:

- Compound growth

- Long-term wealth building

- Retirement preparation

The earlier you start, the longer your money has to grow.

Money Mistake #6: Not Tracking Expenses

You can’t improve what you don’t measure.

Track:

- Groceries

- Dining out

- Entertainment

- Transportation

- Subscriptions

Expense tracking often reveals unnecessary spending.

Money Mistake #7: Lifestyle Inflation

As income increases, many people increase spending at the same pace.

Instead:

- Increase savings

- Increase investments

- Pay down debt

Reward yourself occasionally, but avoid making every raise disappear through higher expenses.

Money Mistake #8: Ignoring Your Credit Score

A good credit score can help when applying for:

- Credit cards

- Auto loans

- Mortgages

- Rental housing

Improve your score by:

- Paying bills on time

- Keeping balances low

- Avoiding unnecessary hard inquiries

Money Mistake #9: Having No Financial Goals

Without goals, saving becomes difficult.

Examples:

- Build a $10,000 emergency fund

- Save for a house

- Pay off student loans

- Invest for retirement

- Save for travel

Break large goals into monthly milestones.

Money Mistake #10: Not Increasing Your Income

Saving is important, but increasing your income can accelerate wealth building.

Ideas include:

- Freelancing

- Side hustles

- Asking for a raise

- Learning new skills

- Starting a small online business

Higher income creates more opportunities to save and invest.

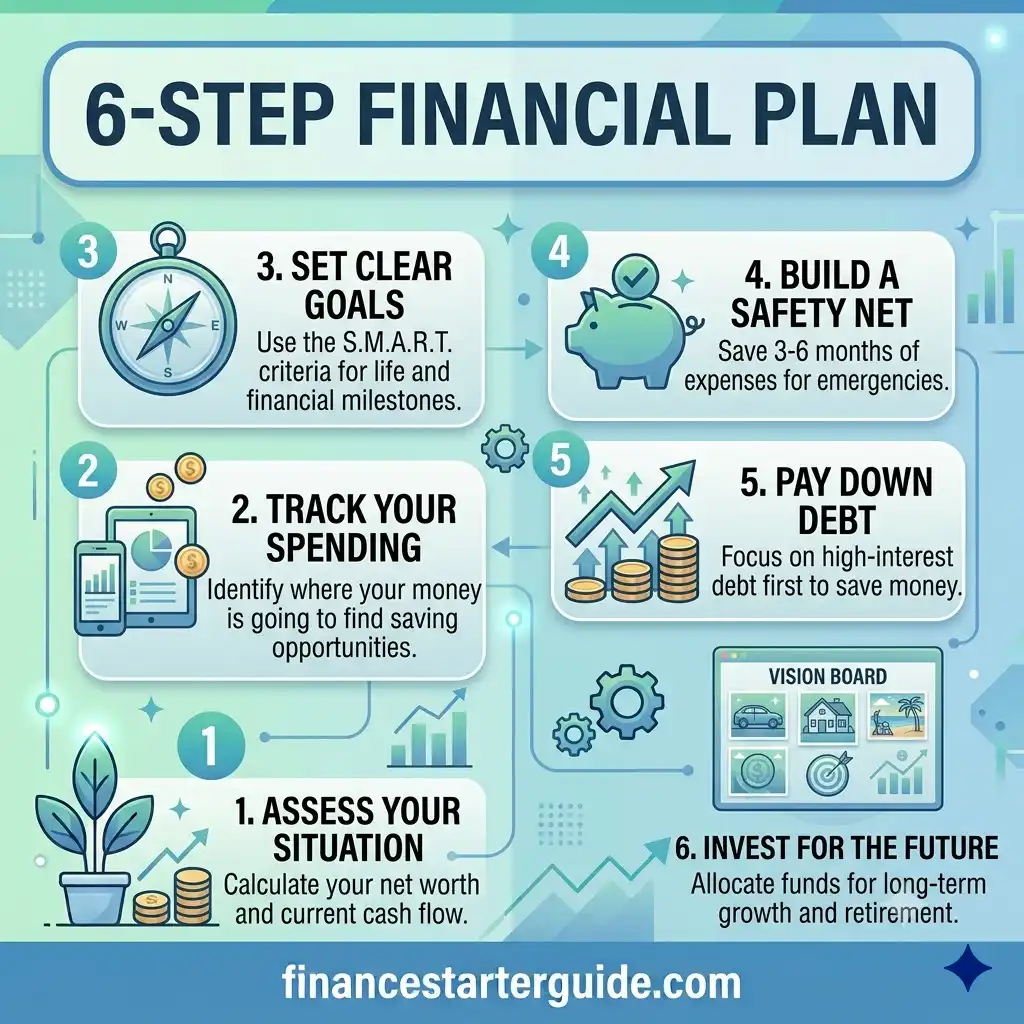

Simple Financial Plan for Your 20s

Step 1

Create a monthly budget.

Step 2

Build an emergency fund.

Step 3

Pay off high-interest debt.

Step 4

Invest consistently.

Step 5

Track expenses weekly.

Step 6

Review your financial goals every month.

Monthly Money Checklist

✔ Review budget

✔ Pay bills on time

✔ Transfer money to savings

✔ Invest consistently

✔ Check subscriptions

✔ Track expenses

✔ Review financial goals

Doing these tasks monthly helps build strong financial habits.

Common Questions

What is the biggest money mistake people make in their 20s?

The biggest mistake is spending more than they earn and failing to save or invest early.

How much should I save in my 20s?

Many financial planners suggest aiming to save at least 20% of your income when possible.

Should I invest before paying off debt?

It depends on the interest rate and your financial situation. High-interest debt is often prioritized before increasing investments.

Is it too early to think about retirement in my 20s?

No. Starting retirement savings early gives your investments more time to grow.

Why is budgeting important in your 20s?

Budgeting helps control spending, reduce debt, and create consistent savings habits.

Conclusion

Your 20s are the perfect time to build healthy financial habits.

Remember these key principles:

- Spend less than you earn.

- Save consistently.

- Invest early.

- Avoid unnecessary debt.

- Track your expenses.

- Keep learning about personal finance.

Small financial decisions made today can have a lasting impact on your future wealth and financial security.

- What Is a Budget? (USA Beginner Guide)

- 50/30/20 Rule Explained

- How to Track Expenses Effectively

- Emergency Fund: How Much Do You Really Need?

- How Millennials Can Build Wealth from Scratch

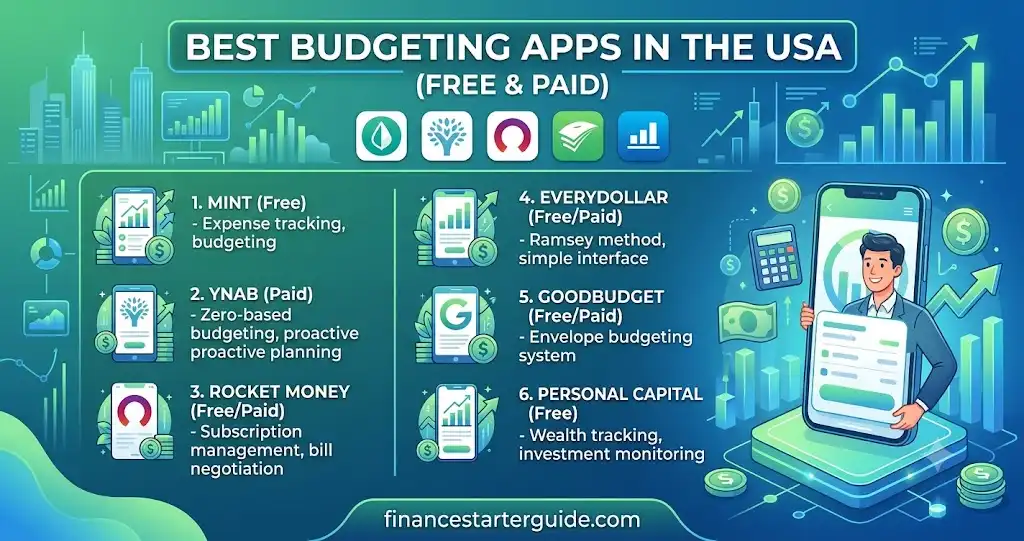

- Best Budgeting Apps in the USA

- How to Save Money Fast on a Low Income

- Best Side Hustles to Save More Money

Disclaimer: This article is for educational and informational purposes only and does not constitute financial, investment, tax, or legal advice.