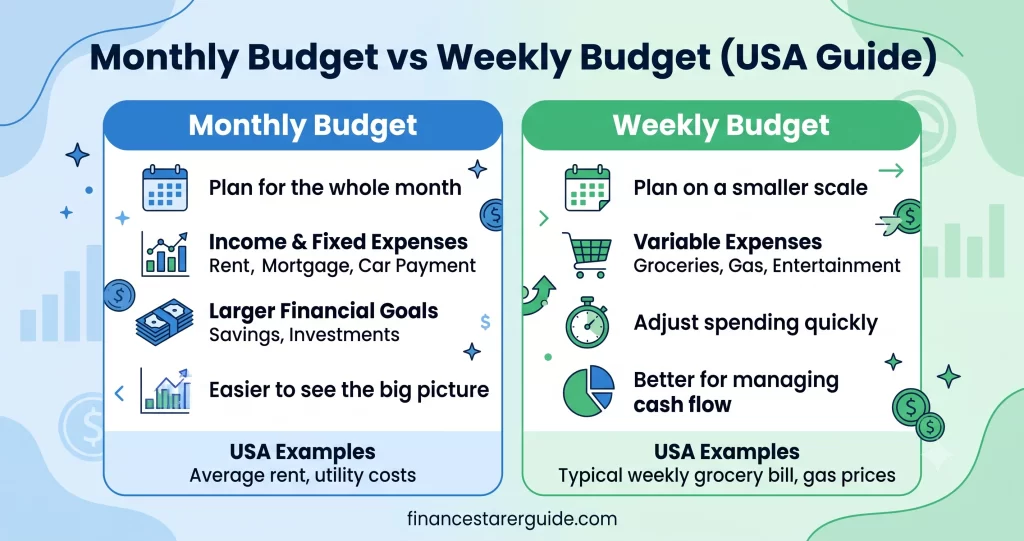

Managing your money successfully starts with choosing a budgeting system that fits your lifestyle. While many financial experts recommend creating a monthly budget, others believe a weekly budget makes it easier to control spending and stay on track.

So, which budgeting method is actually better?

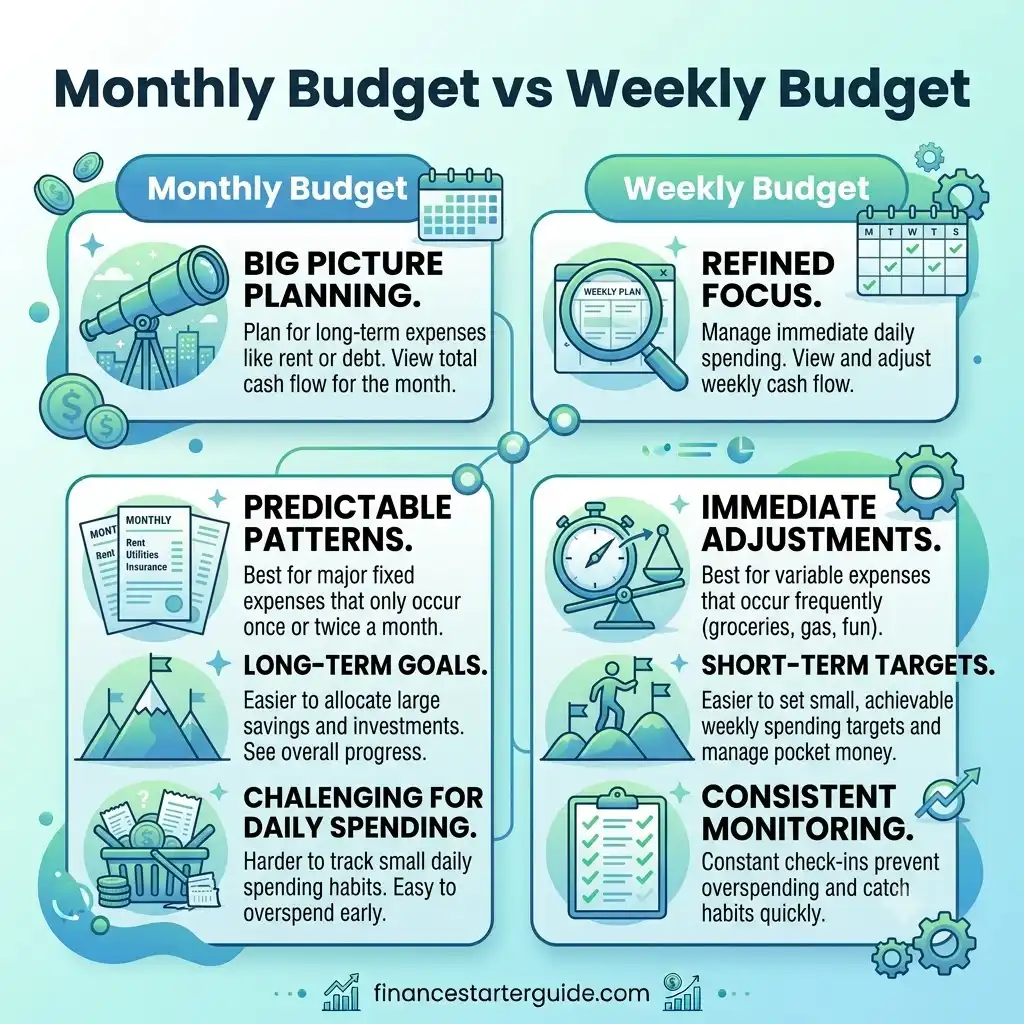

The truth is that both approaches have advantages, and the right choice depends on your income, spending habits, financial goals, and personality. A monthly budget provides a broader overview of your finances, while a weekly budget offers tighter control over day-to-day spending.

In this guide, you’ll learn the differences between monthly and weekly budgeting, the pros and cons of each method, practical examples, and how to decide which budgeting style works best for your situation.

Whether you’re trying to save more money, pay off debt, build an emergency fund, or simply gain better control over your finances, this article will help you choose the right budgeting strategy.

⭐ Quick Answer

Is a Monthly Budget or Weekly Budget Better?

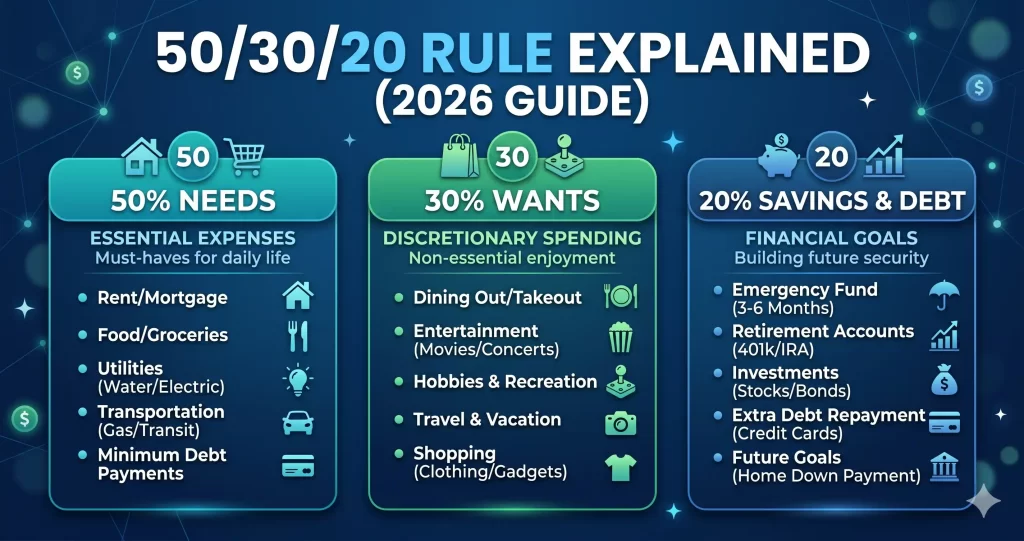

A monthly budget is better for planning fixed expenses such as rent, mortgage, insurance, and utilities because most bills are paid monthly. A weekly budget is better for managing everyday expenses like groceries, dining out, entertainment, and transportation because it helps prevent overspending.

Many people achieve the best results by combining both methods: using a monthly budget for long-term planning and a weekly budget for daily spending.

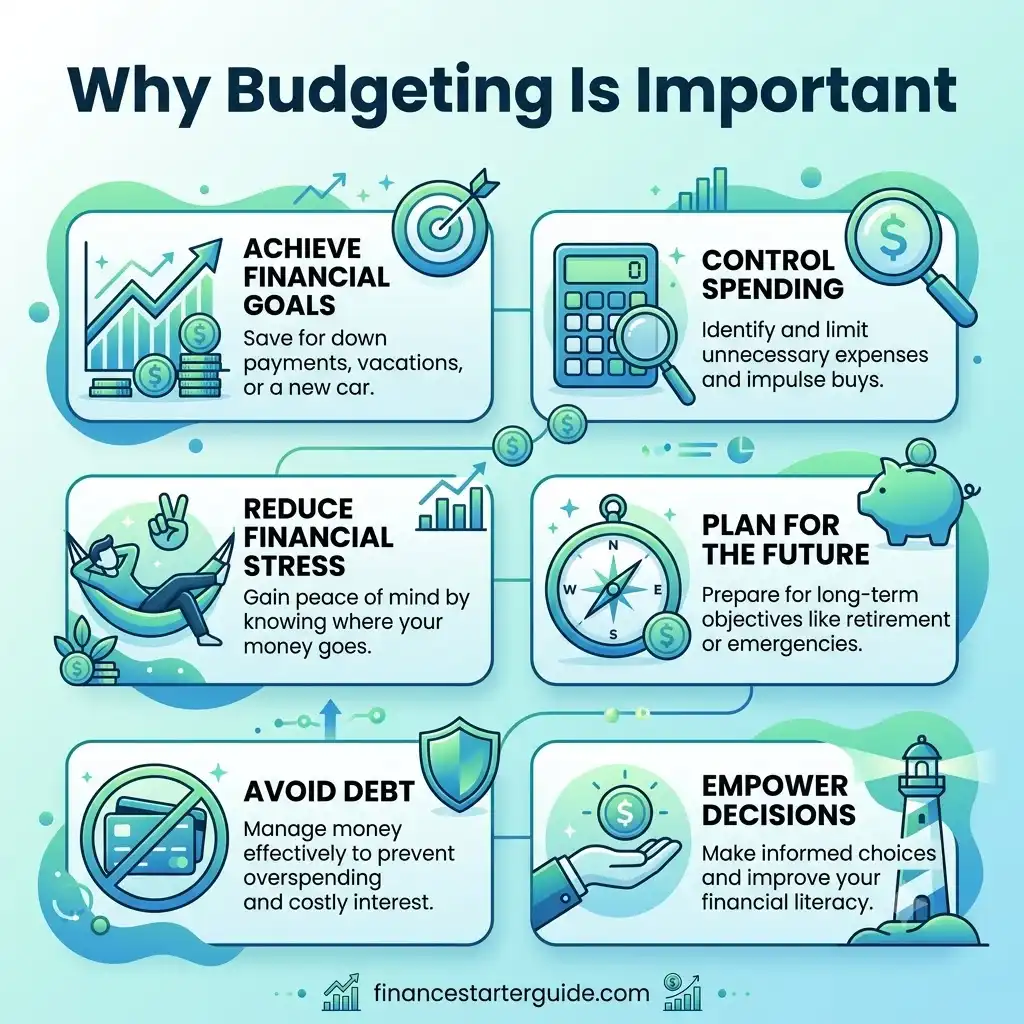

Why Choosing the Right Budget Matters

Budgeting isn’t just about writing numbers on paper. It’s about creating a financial plan that helps you spend intentionally instead of wondering where your money disappeared.

The wrong budgeting method can make managing money feel overwhelming, while the right method makes budgeting almost effortless.

A good budget helps you:

- Understand where your money goes

- Reduce unnecessary spending

- Reach savings goals faster

- Pay bills on time

- Avoid debt

- Prepare for emergencies

- Reduce financial stress

- Build long-term wealth

Regardless of which budgeting system you choose, consistency is far more important than perfection.

What Is a Monthly Budget?

A monthly budget is a financial plan that estimates all of your income and expenses over one calendar month.

Most people receive monthly bills such as:

- Rent or mortgage

- Car payments

- Insurance

- Utilities

- Internet

- Phone bills

- Subscription services

Because these expenses occur monthly, many people find it easiest to organize their finances on a monthly basis.

A monthly budget typically includes:

- Monthly income

- Fixed expenses

- Variable expenses

- Savings

- Debt payments

- Investments

- Remaining balance

It provides a complete picture of your financial situation for the month.

Advantages of a Monthly Budget

1. Matches Most Bills

Most recurring expenses are billed monthly, making it easy to plan ahead.

Examples include:

- Rent

- Mortgage

- Insurance

- Utilities

- Internet

- Loan payments

Planning around these due dates reduces the chance of missed payments.

2. Better Long-Term Planning

Monthly budgets allow you to plan for:

- Vacations

- Retirement savings

- Emergency funds

- Home purchases

- Investments

Instead of focusing only on the next few days, you can make financial decisions based on your entire month’s income.

3. Easier Goal Tracking

Monthly budgeting makes it simple to measure progress toward financial goals.

Examples include:

- Saving $500 each month

- Paying an extra $200 toward debt

- Investing 15% of income

- Building a six-month emergency fund

4. Better Financial Overview

A monthly budget lets you see your complete financial picture at once.

You’ll know:

- Total income

- Total spending

- Savings rate

- Debt payments

- Remaining cash flow

This big-picture perspective helps identify trends that may not be obvious in shorter budgeting periods.

Disadvantages of a Monthly Budget

Although monthly budgeting is popular, it isn’t perfect.

1. Harder to Control Daily Spending

Looking at an entire month’s budget can create a false sense of flexibility.

For example:

You may see that you have $600 allocated for groceries and think you’re doing well after spending $200 in the first week. However, if your spending increases unexpectedly, you could exceed your budget before the month ends.

2. Overspending Happens Gradually

Small purchases often go unnoticed.

Examples:

- Coffee

- Fast food

- Online shopping

- Subscription renewals

Individually, these expenses seem minor, but together they can significantly affect your monthly budget.

3. Less Frequent Check-Ins

Many people only review their monthly budget once or twice during the month.

This delay can make it harder to identify spending problems before they become serious.

What Is a Weekly Budget?

A weekly budget divides your monthly income and expenses into smaller weekly spending limits.

Instead of thinking:

“I have $600 for groceries this month,”

you think:

“I have $150 to spend on groceries this week.”

This smaller time frame makes spending easier to manage.

Weekly budgets are especially useful for:

- Students

- Freelancers

- Gig workers

- Hourly employees

- People living paycheck to paycheck

- Anyone struggling with overspending

Advantages of a Weekly Budget

1. Better Spending Control

Weekly limits help prevent impulse purchases.

Instead of having one large monthly spending allowance, you only focus on the current week.

This reduces the temptation to spend too much too early.

2. Easier to Stay Motivated

Short-term goals feel more achievable.

Completing one successful budgeting week builds momentum for the next.

Small wins encourage long-term financial discipline.

3. Quickly Detects Overspending

Because you’re reviewing your budget every week, you can identify problems early.

If you overspend during one week, you can adjust your spending during the following week instead of waiting until the end of the month.

4. Works Well With Weekly Paychecks

Many hourly workers receive weekly pay.

Weekly budgeting naturally matches their income schedule, making it easier to allocate money for bills, groceries, transportation, and savings.

Disadvantages of a Weekly Budget

Although weekly budgeting provides excellent spending control, it also has limitations.

1. Requires More Frequent Updates

A weekly budget must be reviewed every week.

People who prefer a “set it and forget it” approach may find this time-consuming.

2. Harder to Plan Monthly Bills

Since many expenses are billed monthly, you’ll still need to account for larger payments like rent, insurance, and loan installments.

This requires additional planning.

3. Can Feel Restrictive

Some people dislike having strict weekly spending limits.

If you spend less one week, you may feel tempted to overspend the next.

Maintaining balance is important.

Monthly Budget vs Weekly Budget: Side-by-Side Comparison

| Feature | Monthly Budget | Weekly Budget |

|---|---|---|

| Planning Period | One month | One week |

| Best For | Long-term planning | Daily spending control |

| Bill Management | Excellent | Moderate |

| Expense Tracking | Moderate | Excellent |

| Overspending Prevention | Good | Excellent |

| Goal Tracking | Excellent | Good |

| Time Required | Low | Moderate |

| Best Income Type | Monthly salary | Weekly or variable income |

This comparison shows that neither method is universally better—they simply serve different purposes.

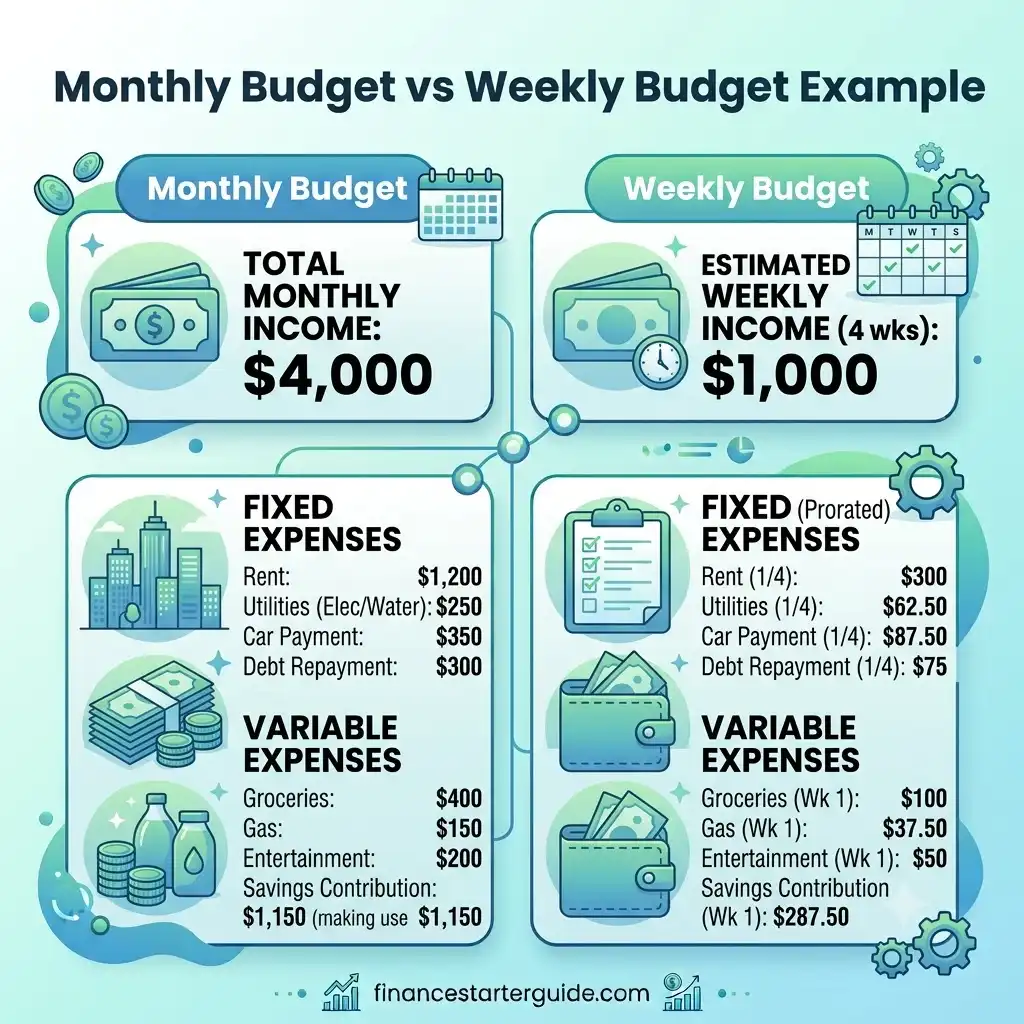

Real-Life Budgeting Example: Monthly Budget

Let’s imagine Sarah, who earns $4,000 per month after taxes.

She uses a monthly budget because most of her bills are due once a month.

Sarah’s Monthly Budget

| Category | Budget |

|---|---|

| Income | $4,000 |

| Rent | $1,200 |

| Utilities | $250 |

| Groceries | $500 |

| Transportation | $300 |

| Insurance | $180 |

| Entertainment | $250 |

| Dining Out | $150 |

| Savings | $800 |

| Debt Payments | $220 |

| Miscellaneous | $150 |

Sarah reviews her budget once every week but plans everything at the beginning of the month.

Why It Works

- Bills are organized

- Savings happen automatically

- Long-term planning is easier

- Less time spent budgeting

Real-Life Budgeting Example: Weekly Budget

Now consider James, who works as a freelancer.

His income varies every week.

Instead of budgeting monthly, he divides his spending into weekly limits.

James’ Weekly Budget

| Category | Weekly Budget |

|---|---|

| Groceries | $125 |

| Gas | $60 |

| Dining Out | $40 |

| Entertainment | $35 |

| Personal Spending | $40 |

| Savings | $100 |

Every Sunday, James checks his spending before planning the next week.

Why It Works

- Easier to adjust when income changes

- Better spending control

- Less chance of running out of money

- Helps avoid impulse purchases

Which Budget Is Better for Different People?

The best budgeting method depends on your financial situation and lifestyle.

Best for Salaried Employees

If you receive a fixed monthly paycheck, a monthly budget is usually the better option.

Why?

- Matches bill due dates

- Easier planning

- Consistent income

- Better savings strategy

Best for Hourly Workers

Hourly workers often receive weekly or biweekly pay.

A weekly budget helps:

- Control spending

- Adjust to varying income

- Prevent overspending before payday

Best for Freelancers

Freelancers often experience inconsistent income.

The ideal approach is:

- Monthly planning

- Weekly spending reviews

This combination provides flexibility while still preparing for larger monthly expenses.

Best for Students

Students generally benefit from weekly budgeting because:

- Spending is easier to monitor

- Smaller budgets feel more manageable

- Helps stretch limited income

Best for Families

Families usually have many monthly bills.

Examples:

- Mortgage

- Utilities

- Childcare

- Insurance

- School expenses

A monthly budget makes it easier to organize these recurring expenses.

Weekly check-ins can then be used to monitor grocery and entertainment spending.

Best for People Paying Off Debt

If you’re aggressively paying off debt, combining both methods works well.

Monthly budgeting helps you schedule debt payments, while weekly budgeting keeps discretionary spending under control so you can apply more money toward your balances.

Which Budget Helps You Save More Money?

Many people ask which method leads to greater savings.

The answer depends on your spending habits.

Monthly Budget Advantages for Saving

- Easier to set monthly savings goals

- Better retirement planning

- Simplifies emergency fund contributions

- Supports long-term investing

Weekly Budget Advantages for Saving

- Reduces impulse purchases

- Encourages mindful spending

- Makes it easier to identify unnecessary expenses

- Helps you adjust quickly if you overspend

Winner: Weekly budgeting often helps people save more if overspending is their biggest challenge.

Which Budget Is Easier to Maintain?

Monthly Budget

Easier Because:

- Created once per month

- Less frequent updates

- Simple to maintain

- Matches most bills

Weekly Budget

Easier Because:

- Smaller spending goals

- Regular accountability

- Easier to notice problems

However, it requires more discipline because you need to review it every week.

Common Budgeting Mistakes

No matter which budgeting method you choose, avoid these common mistakes.

1. Not Tracking Expenses

A budget only works if you compare it with your actual spending.

Use a spreadsheet, budgeting app, or notebook to record purchases.

2. Forgetting Annual Expenses

Examples include:

- Car registration

- Holiday shopping

- Insurance renewals

- Home maintenance

Plan for these by creating sinking funds.

3. Setting Unrealistic Limits

If you completely eliminate entertainment or dining out, you’re more likely to abandon your budget.

Build flexibility into your plan.

4. Ignoring Emergency Savings

Unexpected expenses happen.

Aim to save three to six months of essential living expenses over time.

5. Giving Up After One Bad Week

Everyone overspends occasionally.

Instead of quitting, adjust your budget and continue.

Consistency beats perfection.

Can You Combine Monthly and Weekly Budgets?

Yes—and for many people, this is the most effective strategy.

Here’s how:

Step 1

Create a monthly budget for:

- Rent or mortgage

- Utilities

- Insurance

- Savings

- Debt payments

- Investments

Step 2

Break your variable expenses into weekly amounts.

For example:

| Monthly Category | Weekly Limit |

|---|---|

| Groceries ($600) | $150 |

| Dining Out ($200) | $50 |

| Entertainment ($160) | $40 |

| Gas ($240) | $60 |

This approach gives you the long-term planning benefits of a monthly budget while helping you control everyday spending.

Expert Tips to Make Either Budget Work

Follow these practical tips regardless of which method you choose:

- Pay yourself first by automating savings.

- Review your spending at the same time each week.

- Track every purchase, even small ones.

- Use separate savings accounts for major goals.

- Keep an emergency fund for unexpected costs.

- Revisit your budget whenever your income changes.

- Celebrate milestones to stay motivated.

Monthly Budget vs Weekly Budget: Final Comparison

| Category | Monthly Budget | Weekly Budget |

|---|---|---|

| Best for Fixed Bills | ⭐⭐⭐⭐⭐ | ⭐⭐⭐ |

| Best for Daily Spending | ⭐⭐⭐ | ⭐⭐⭐⭐⭐ |

| Easier to Create | ⭐⭐⭐⭐⭐ | ⭐⭐⭐⭐ |

| Prevents Overspending | ⭐⭐⭐ | ⭐⭐⭐⭐⭐ |

| Helps Reach Savings Goals | ⭐⭐⭐⭐⭐ | ⭐⭐⭐⭐ |

| Best for Beginners | ⭐⭐⭐⭐ | ⭐⭐⭐⭐ |

| Best Overall | ⭐⭐⭐⭐⭐ | ⭐⭐⭐⭐ |

Key Takeaway

If you have a stable monthly income and predictable bills, a monthly budget offers the best long-term financial planning. If your main challenge is controlling day-to-day spending or your income varies, a weekly budget provides stronger short-term control.

For many people, combining both methods delivers the best results.

Frequently Asked Questions

Is a monthly budget better than a weekly budget?

A monthly budget is better for planning fixed expenses such as rent, mortgage, insurance, and utilities because most bills are paid monthly. A weekly budget is better for controlling day-to-day spending and preventing overspending. Many people benefit from using both methods together.

Should beginners use a monthly or weekly budget?

Beginners can succeed with either approach. A monthly budget offers a clear overview of finances, while a weekly budget makes it easier to monitor spending habits. If you’re new to budgeting, starting with a monthly budget and reviewing it weekly is often the most practical strategy.

Can I use both a monthly and weekly budget?

Yes. Many financial experts recommend creating a monthly budget for income, bills, savings, and debt payments, then breaking variable expenses such as groceries, gas, and entertainment into weekly spending limits.

Which budgeting method helps save more money?

A weekly budget often helps reduce impulse spending because you focus on smaller spending limits. However, a monthly budget is better for planning long-term savings goals. Combining both methods usually produces the best results.

How often should I review my budget?

Review your spending every week and perform a complete budget review at the end of each month. Regular reviews help you identify problems early and adjust your spending before small issues become larger ones.

What expenses should always be included in a budget?

Every budget should include:

- Income

- Housing costs

- Utilities

- Transportation

- Groceries

- Insurance

- Debt payments

- Savings

- Emergency fund contributions

- Entertainment

- Miscellaneous expenses

Which Budgeting Method Should You Choose?

Choosing the right budgeting method depends on your financial situation rather than following a one-size-fits-all approach.

Choose a Monthly Budget If You:

- Receive a fixed monthly salary

- Want a complete financial overview

- Have mostly monthly bills

- Focus on long-term savings and investing

- Prefer updating your budget less frequently

Choose a Weekly Budget If You:

- Struggle with overspending

- Receive weekly or variable income

- Want tighter control over daily expenses

- Prefer short-term financial goals

- Need frequent accountability

Combine Both If You Want the Best Results

A hybrid budgeting system gives you the strengths of both methods:

- Plan all income and fixed bills monthly.

- Divide groceries, dining, transportation, and entertainment into weekly limits.

- Review spending every Sunday.

- Adjust your next week’s budget based on actual spending.

This approach keeps your long-term financial plan organized while helping you stay disciplined with everyday purchases.

Monthly Budget Review Checklist

At the end of every month, ask yourself these questions:

- Did I stay within my planned budget?

- Which categories exceeded my spending limit?

- Did I save the amount I planned?

- Did I pay all bills on time?

- Did I make progress toward paying off debt?

- Did any unexpected expenses occur?

- What should I improve next month?

Keeping a simple monthly review helps turn budgeting into a lasting habit.

Conclusion

There is no universal winner in the debate between a monthly budget and a weekly budget. The best budgeting system is the one you can consistently follow.

A monthly budget provides a complete picture of your finances, making it ideal for managing fixed bills, planning savings, and working toward long-term financial goals. A weekly budget, on the other hand, helps you stay focused on everyday spending and makes it easier to avoid impulse purchases.

For most people, combining these two approaches offers the greatest benefit. Use a monthly budget to organize your income, bills, savings, and debt payments, then break your variable expenses into weekly spending limits. This simple strategy creates better financial awareness, improves spending habits, and makes achieving your financial goals much more manageable.

Remember that successful budgeting isn’t about restricting yourself—it’s about making intentional decisions with your money so you can enjoy financial security and peace of mind.

- How to Create a Monthly Budget That Actually Works

- Best Free Budget Templates for Beginners (USA)

- How to Track Expenses Effectively (Free Methods)

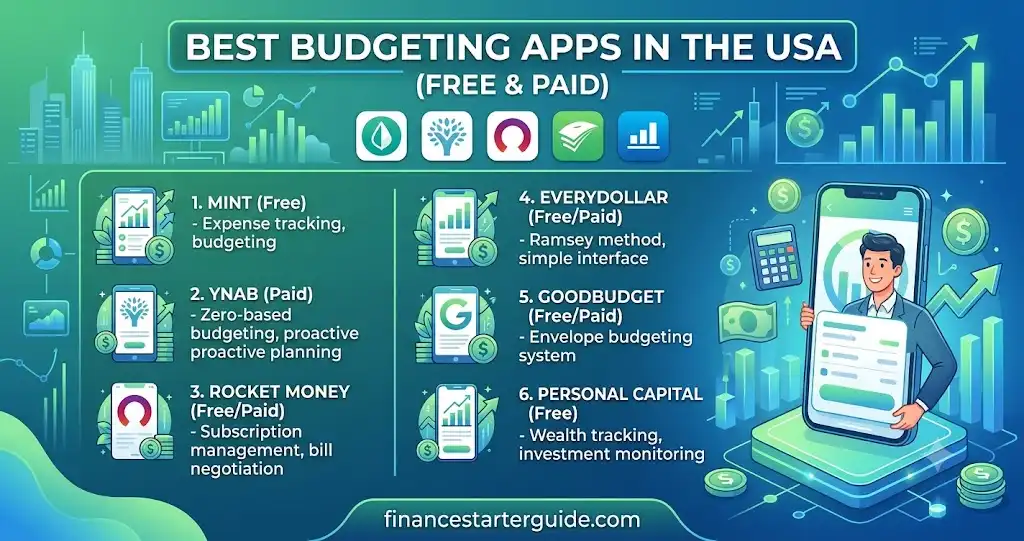

- Best Budgeting Apps in the USA

- How to Increase Your Savings Without Increasing Income

- Emergency Fund: How Much Do You Really Need?

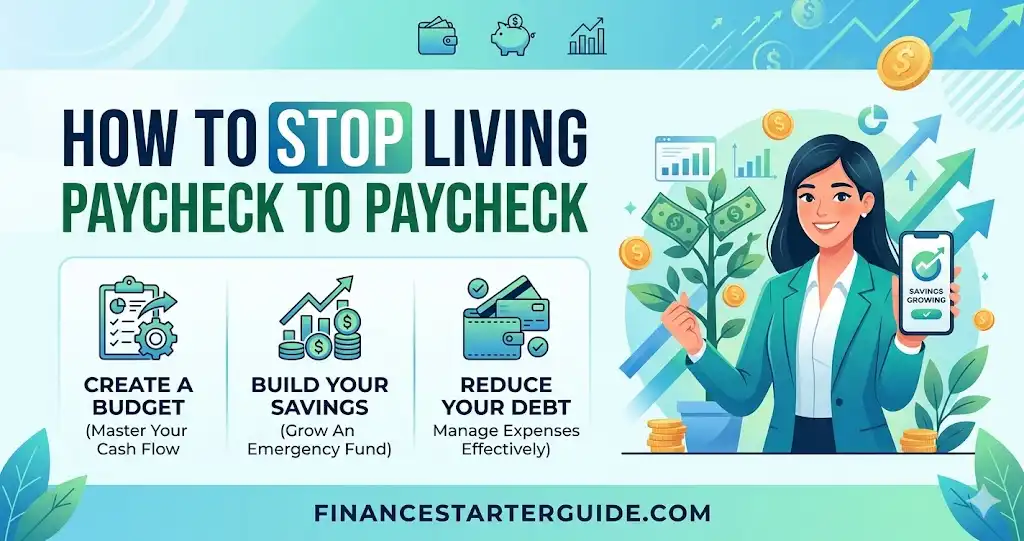

- How to Stop Living Paycheck to Paycheck

- Best Financial Tools & Apps in the USA

- Best Side Hustles to Save More Money (USA)

- How to Build Good Financial Habits That Stick

Disclaimer: This article is for educational and informational purposes only and does not constitute financial, investment, tax, or legal advice.