If you’re struggling with debt, you’re not alone.

Millions of Americans carry credit card balances, personal loans, student loans, and other debts. The good news is that there are proven methods to pay off debt faster.

Two of the most popular strategies are:

Both methods work, but they take different approaches.

In this guide, you’ll learn exactly how each strategy works, their advantages and disadvantages, and which one may be best for your financial situation.

🔥 Quick Answer

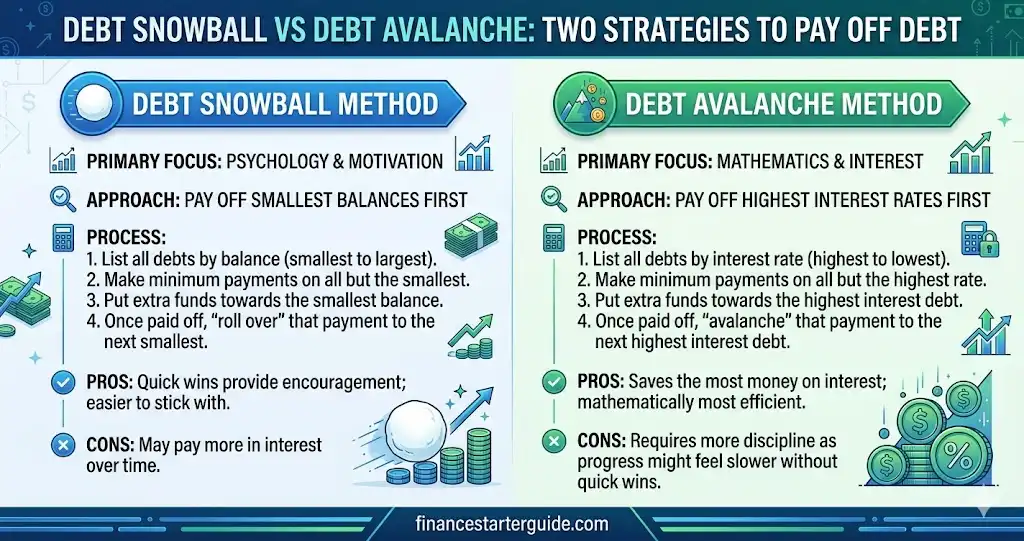

The Debt Snowball Method focuses on paying off the smallest debts first for quick wins, while the Debt Avalanche Method targets debts with the highest interest rates first to save the most money. The best method depends on whether you need motivation or maximum interest savings.

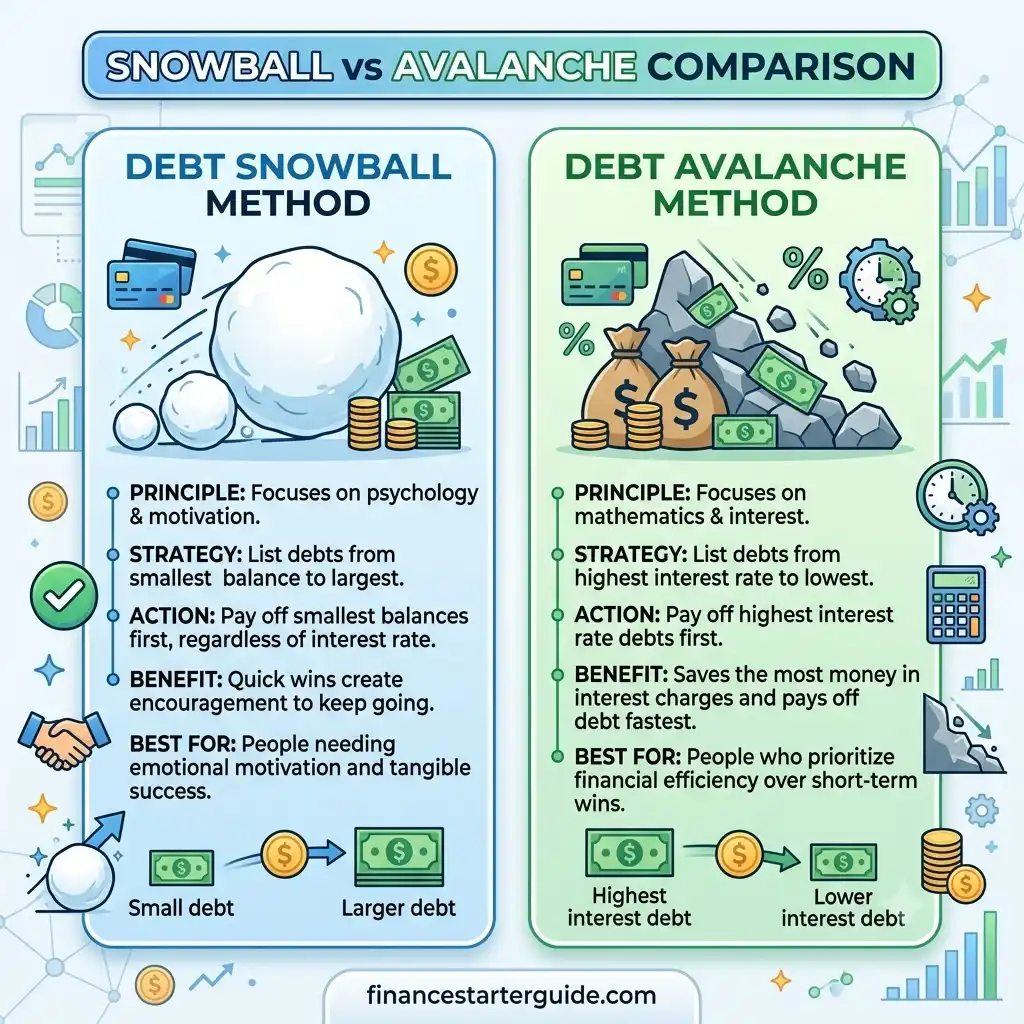

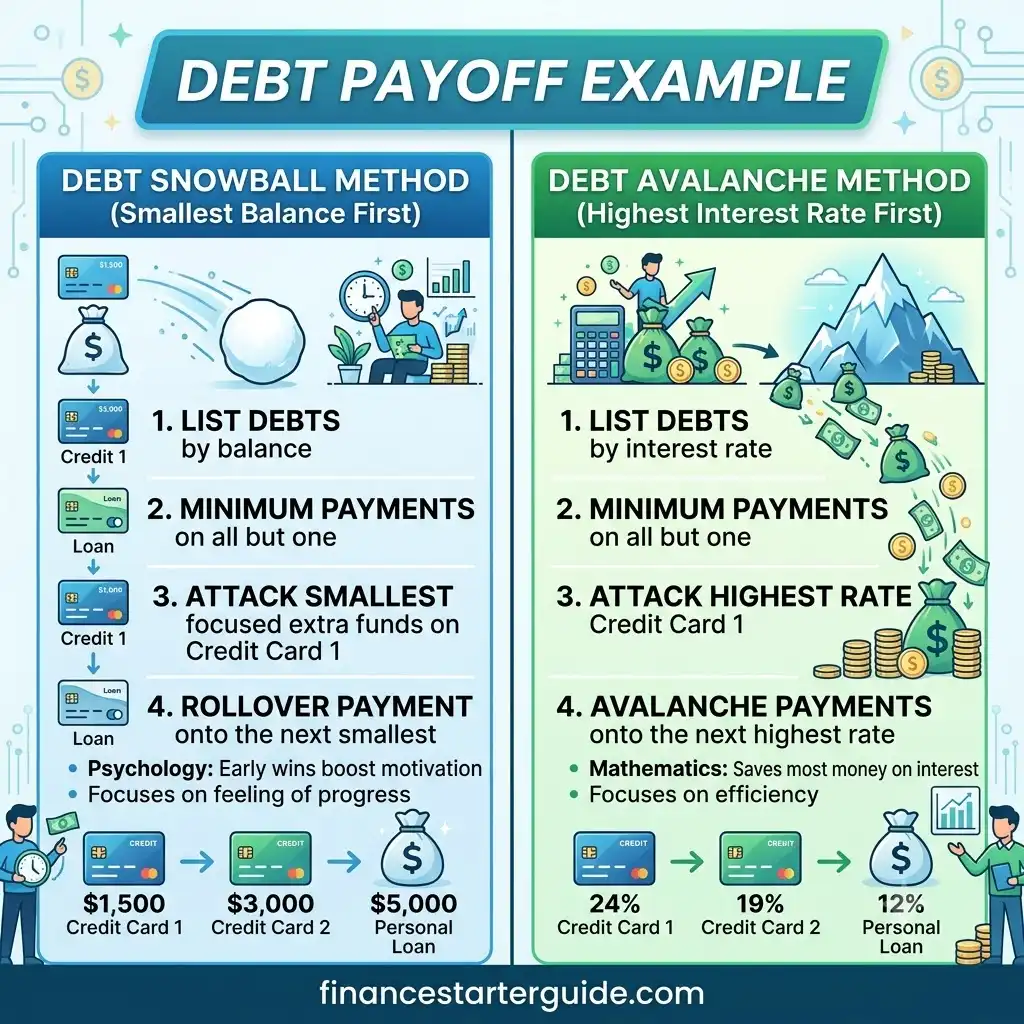

What Is the Debt Snowball Method?

The Debt Snowball Method was popularized by financial expert Dave Ramsey.

The concept is simple:

- List all debts from smallest balance to largest balance.

- Make minimum payments on all debts.

- Put extra money toward the smallest debt.

- Once that debt is paid off, roll the payment into the next smallest debt.

As each debt disappears, your momentum grows like a snowball rolling downhill.

Example of Debt Snowball

| Debt | Balance | Interest Rate |

|---|---|---|

| Credit Card A | $500 | 25% |

| Personal Loan | $3,000 | 10% |

| Auto Loan | $10,000 | 6% |

Using the snowball method:

- Pay off Credit Card A first.

- Then attack the Personal Loan.

- Finally pay off the Auto Loan.

Benefits of Debt Snowball

1. Quick Wins

Small debts disappear quickly.

This creates motivation and confidence.

2. Easier to Stay Consistent

People often stick with the plan longer because they see progress faster.

3. Builds Positive Financial Habits

Small victories encourage long-term discipline.

Drawbacks of Debt Snowball

1. Higher Interest Costs

You may pay more interest over time.

2. Slower Total Savings

The highest-interest debt isn’t always tackled first.

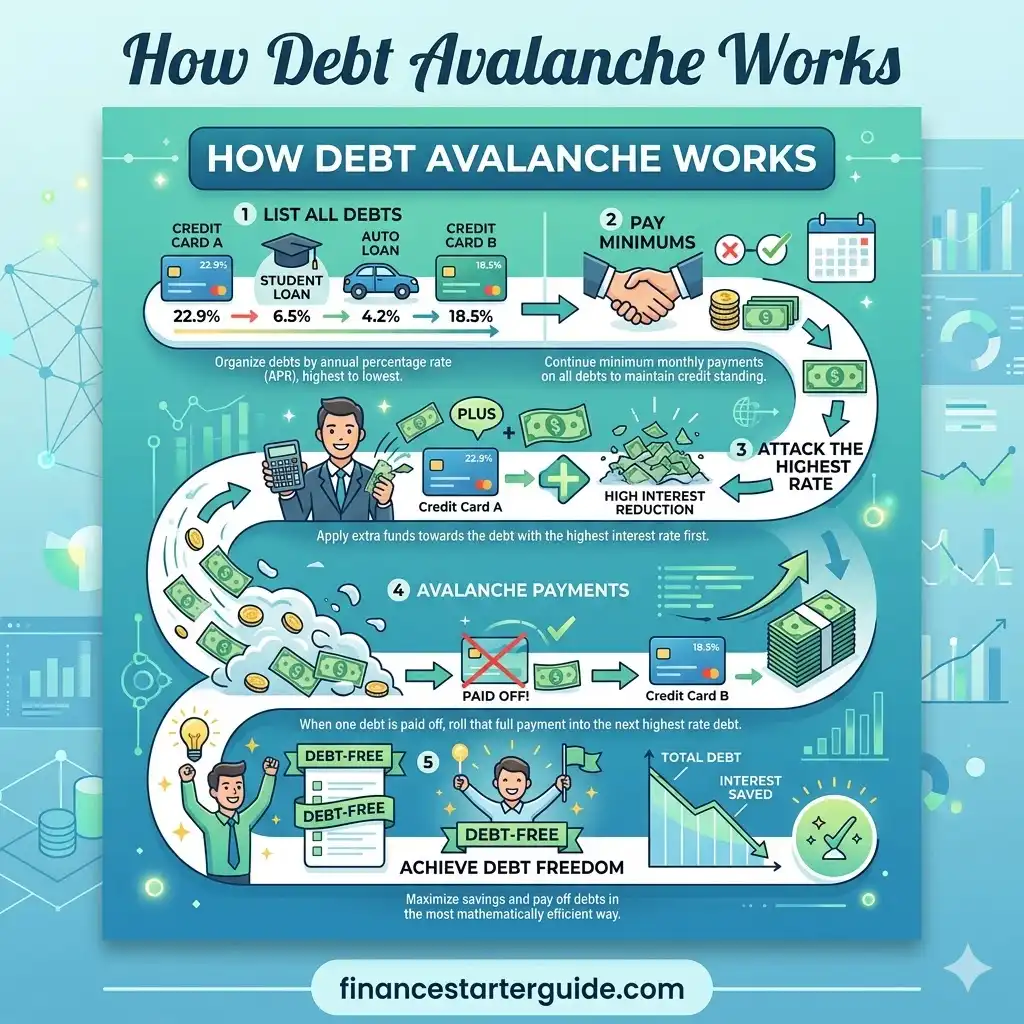

What Is the Debt Avalanche Method?

The Debt Avalanche Method focuses on interest rates rather than balances.

Steps:

- List debts from highest interest rate to lowest.

- Pay minimums on all debts.

- Put extra money toward the highest-interest debt.

- Once paid off, move to the next highest rate.

This strategy mathematically saves the most money.

Example of Debt Avalanche

| Debt | Balance | Interest Rate |

|---|---|---|

| Credit Card A | $5,000 | 29% |

| Personal Loan | $2,000 | 12% |

| Auto Loan | $10,000 | 6% |

Using the avalanche method:

- Pay Credit Card A first.

- Then Personal Loan.

- Then Auto Loan.

Benefits of Debt Avalanche

1. Saves More Money

High-interest debts disappear first.

2. Faster Financial Efficiency

More money goes toward principal instead of interest.

3. Mathematically Superior

Most financial experts prefer avalanche because it minimizes total borrowing costs.

Drawbacks of Debt Avalanche

1. Less Motivation

Large debts can take months before you see a payoff.

2. Harder for Some People

Without quick wins, some people quit.

Debt Snowball vs Debt Avalanche: Side-by-Side Comparison

| Factor | Debt Snowball | Debt Avalanche |

|---|---|---|

| Focus | Smallest Balance | Highest Interest |

| Motivation | High | Moderate |

| Interest Savings | Lower | Higher |

| Speed of Small Wins | Fast | Slow |

| Best For | Motivation | Saving Money |

| Psychological Benefit | Excellent | Moderate |

Which Method Pays Off Debt Faster?

Many people assume the avalanche method always pays off debt faster.

In reality:

- Avalanche usually saves more money.

- Snowball often keeps people motivated.

- Consistency matters more than perfection.

A strategy that you follow consistently is better than a perfect strategy you abandon.

Real-Life Example

Imagine you have:

- Credit Card Debt: $2,000 at 28%

- Personal Loan: $5,000 at 12%

- Auto Loan: $8,000 at 6%

Snowball Method

You pay the smallest balance first.

Result:

- Faster motivation

- More psychological wins

Avalanche Method

You attack the 28% credit card first.

Result:

- Less interest paid

- More money saved

The Psychology of Debt Payoff

Personal finance is not only math.

It’s behavior.

Many people know what they should do but struggle to stay motivated.

This is why the snowball method has become so popular.

Research in behavioral finance suggests that visible progress often encourages people to continue pursuing long-term goals.

When Debt Snowball Is Better

Choose Debt Snowball if:

✅ You need motivation

✅ You have many small debts

✅ You’ve struggled with debt repayment before

✅ You want quick wins

When Debt Avalanche Is Better

Choose Debt Avalanche if:

✅ You want maximum savings

✅ You have high-interest credit card debt

✅ You’re disciplined with money

✅ You care about efficiency

Hybrid Debt Strategy

Many people combine both methods.

Example:

- Pay off one or two small debts for motivation.

- Switch to avalanche for maximum savings.

This hybrid approach offers both momentum and efficiency.

How to Start Paying Off Debt Today

Step 1: List Every Debt

Write down:

- Creditor

- Balance

- Interest Rate

- Minimum Payment

Step 2: Choose Your Strategy

Pick Snowball or Avalanche.

Step 3: Create a Budget

Find extra money each month.

Step 4: Increase Income

Consider:

- Freelancing

- Side hustles

- Selling unused items

Step 5: Stay Consistent

Consistency beats intensity.

Common Debt Payoff Mistakes

❌ Only Paying Minimum Payments

This keeps you in debt longer.

❌ Taking On New Debt

Avoid adding new balances.

❌ Ignoring Interest Rates

Understand how much debt costs.

❌ Not Tracking Progress

Regular reviews help maintain momentum.

How Much Money Can You Save?

Suppose you owe:

- $10,000 at 25%

- $5,000 at 10%

Using Avalanche instead of Snowball could save hundreds or even thousands of dollars depending on repayment speed.

The larger the debt, the bigger the potential savings.

FAQs

What is the difference between Debt Snowball and Debt Avalanche?

Debt Snowball focuses on the smallest balance first, while Debt Avalanche targets the highest interest rate first.

Which method saves more money?

Debt Avalanche usually saves more money because high-interest debts are paid first.

Which method is best for beginners?

Debt Snowball is often easier for beginners because it provides quick wins.

Does Debt Snowball really work?

Yes. Many people successfully eliminate debt using the snowball strategy.

Should I combine both methods?

A hybrid approach can be effective if you want motivation and savings.

Conclusion

Both Debt Snowball and Debt Avalanche can help you become debt-free.

Choose Debt Snowball if motivation is your biggest challenge.

Choose Debt Avalanche if saving money is your top priority.

The most important factor isn’t which strategy you choose—it’s sticking with it until every debt is gone.

- What Is a Credit Score?

- Credit Utilization Explained

- Best Personal Loans for Beginners

- How to Stop Living Paycheck to Paycheck

- Emergency Fund Guide

- 50/30/20 Rule Explained

Disclaimer: This article is for educational and informational purposes only and does not constitute financial, investment, tax, or legal advice.