Many people believe they need a higher salary before they can save more money. While earning more can certainly help, it’s not the only way to build savings.

In reality, improving your financial habits and making smarter spending decisions can significantly increase your savings even if your income stays exactly the same.

Whether you’re living paycheck to paycheck, trying to build an emergency fund, or saving for a home, this guide will show you practical ways to save more without asking for a raise or taking on another job.

You’ll learn how to identify hidden spending leaks, create a realistic budget, automate savings, reduce monthly expenses, and build long-term financial security.

🔥 Quick Answer

How Can You Increase Your Savings Without Increasing Income?

You can increase your savings without earning more by:

- Creating a realistic monthly budget

- Tracking every expense

- Paying yourself first

- Reducing unnecessary subscriptions

- Planning meals

- Shopping with a list

- Negotiating monthly bills

- Automating savings

- Avoiding impulse purchases

- Setting clear savings goals

Small improvements repeated consistently can dramatically increase your savings over time.

Why Saving More Doesn’t Always Require More Income

Many households receive raises but still struggle financially because their spending rises along with their income.

This is called lifestyle inflation.

Instead of focusing only on earning more, focus on improving how you manage the money you already have.

Benefits include:

- Better financial security

- Reduced stress

- Faster emergency fund growth

- Less debt

- Greater financial independence

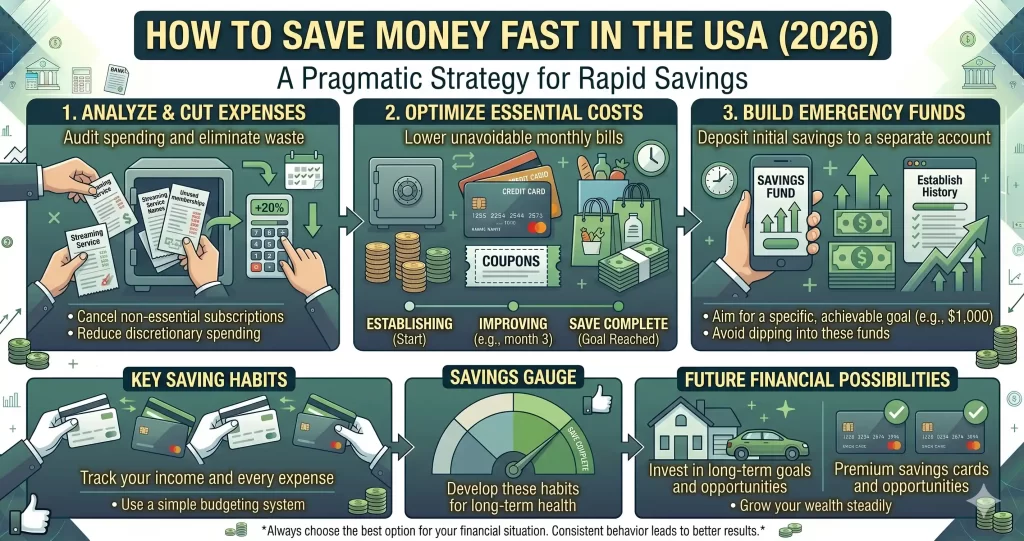

Step 1: Create a Budget That Works

A budget gives every dollar a purpose.

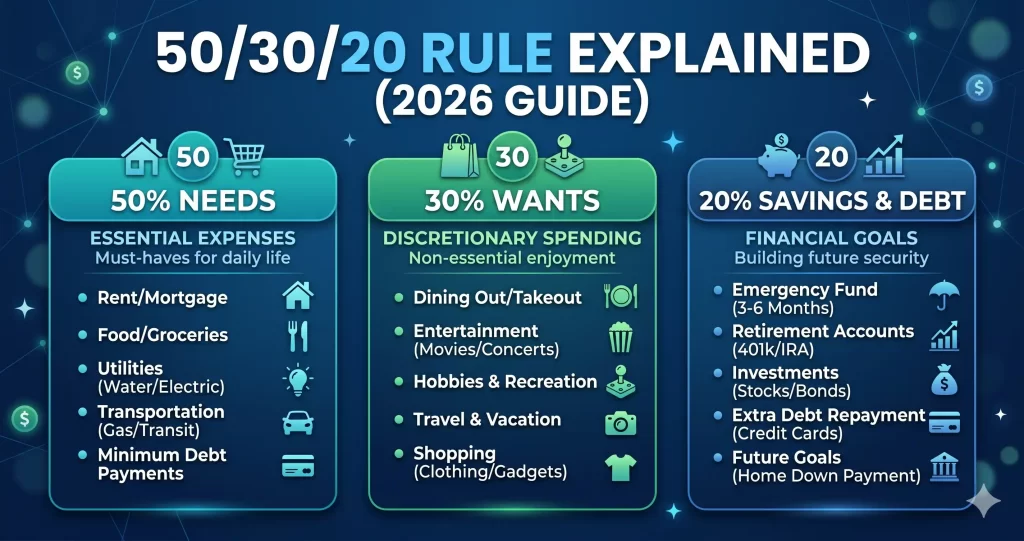

Popular budgeting methods include:

- 50/30/20 Rule

- Zero-Based Budget

- Envelope Budget

A good budget helps you:

- Spend intentionally

- Prevent overspending

- Increase savings automatically

- Reach financial goals faster

Simple Example

Monthly Income: $3,000

Needs: $1,500

Wants: $900

Savings: $600

Review your budget every month and adjust it as your expenses change.

Step 2: Track Every Dollar

Many people don’t know where their money goes.

For one month, record every expense, including:

- Coffee

- Snacks

- Online shopping

- Streaming services

- Dining out

- Transportation

Tracking expenses often reveals hundreds of dollars in unnecessary spending each month.

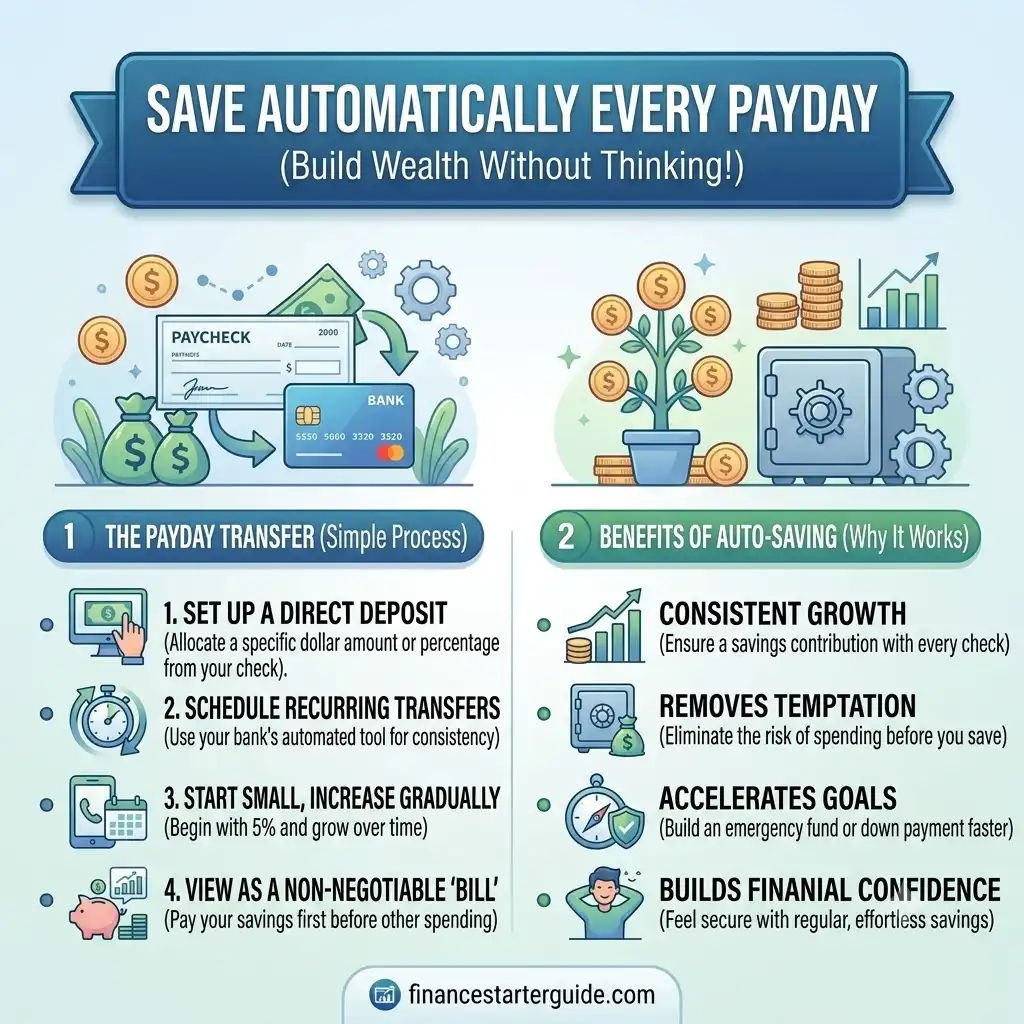

Step 3: Pay Yourself First

One of the simplest savings strategies is paying yourself before paying for optional spending.

Example:

Payday arrives.

Immediately transfer:

- 10%

- 15%

- or 20%

into savings.

Spend what’s left.

Automating this transfer removes the temptation to spend the money first.

Step 4: Reduce Monthly Bills

Review every recurring expense.

Examples:

- Internet

- Mobile phone

- Insurance

- Streaming services

- Gym memberships

Ask providers whether they offer:

- Loyalty discounts

- Promotional pricing

- Lower-cost plans

Even small monthly reductions add up over a year.

Step 5: Stop Lifestyle Inflation

Receiving a raise doesn’t mean every expense should increase.

Instead of upgrading:

- Car

- Apartment

- Electronics

- Dining habits

Use the additional room in your budget to strengthen savings and investments.

Step 6: Meal Plan and Cook More Often

Food is one of the easiest areas to reduce spending.

Try these habits:

- Plan weekly meals

- Shop with a grocery list

- Buy store brands

- Cook larger portions

- Pack lunch for work

Preparing meals at home more often can reduce monthly food costs while still allowing room for occasional dining out.

Step 7: Cancel Unused Subscriptions

Review all recurring subscriptions.

Examples:

- Streaming platforms

- Music services

- Fitness apps

- Cloud storage

- Premium memberships

Ask yourself:

“Did I use this last month?”

If not, consider canceling or downgrading.

Step 8: Avoid Impulse Purchases

Impulse buying can quietly drain your budget.

Try the 24-hour rule:

Before buying something you didn’t plan for, wait at least one day.

Often, the urge passes and you save money.

Other helpful habits include:

- Shopping with a list

- Avoiding shopping when bored

- Removing saved payment methods from online stores

Step 9: Set Clear Savings Goals

Saving is easier when you know what you’re saving for.

Examples:

- $1,000 emergency fund

- Vacation

- Home down payment

- New car

- Retirement

- Education

Break larger goals into monthly targets.

Step 10: Automate Savings

Automation makes saving effortless.

Schedule automatic transfers:

- Weekly

- Bi-weekly

- Monthly

Treat savings like any other important bill.

Step 11: Build Better Shopping Habits

Before every purchase:

✔ Compare prices

✔ Use coupons

✔ Buy only what you need

✔ Wait for sales when appropriate

✔ Avoid emotional shopping

Making thoughtful purchasing decisions over time can significantly improve your savings rate.

Step 12: Review Your Finances Every Month

Once each month:

- Review your budget

- Check savings progress

- Identify unnecessary expenses

- Adjust financial goals

Monthly reviews help you stay accountable and make steady improvements.

Monthly Savings Checklist

✔ Follow your budget

✔ Save before spending

✔ Track expenses

✔ Avoid impulse purchases

✔ Review subscriptions

✔ Cook more meals

✔ Pay bills on time

✔ Review savings goals

Common Mistakes That Reduce Savings

Avoid these habits:

❌ Spending without a budget

❌ Ignoring subscriptions

❌ Shopping emotionally

❌ Carrying credit card balances

❌ Lifestyle inflation

❌ Not tracking expenses

❌ Waiting to save what’s left

❌ Setting unrealistic financial goals

Replacing one bad habit at a time leads to more sustainable progress.

FAQs

Can I save more money without earning more?

Yes. Reducing unnecessary expenses, budgeting, automating savings, and improving spending habits can increase savings without increasing income.

What is the fastest way to save more money?

Track your spending, create a budget, eliminate unnecessary expenses, and automate savings immediately after payday.

How much should I save each month?

A common goal is to save at least 20% of your income, but any consistent amount is a positive step.

Why do people struggle to save money?

Common reasons include lack of budgeting, impulse spending, lifestyle inflation, and not setting clear savings goals.

Is budgeting really necessary?

Yes. A budget helps you control spending, prioritize savings, and make better financial decisions.

Conclusion

Increasing your savings isn’t always about earning more it’s about making the most of what you already have.

Start by:

- Creating a realistic budget

- Tracking every expense

- Automating your savings

- Reducing unnecessary spending

- Avoiding lifestyle inflation

- Reviewing your finances regularly

Small changes repeated consistently can lead to significant financial progress over time.

- What Is a Budget? (USA Beginner Guide)

- 50/30/20 Rule Explained

- How to Track Expenses Effectively

- Best Budgeting Apps in the USA

- How to Build Good Financial Habits That Stick

- Emergency Fund: How Much Do You Really Need?

- Best Side Hustles to Save More Money

- How to Avoid Common Money Mistakes in Your 20s

Disclaimer: This article is for educational and informational purposes only and does not constitute financial, investment, tax, or legal advice.